In This Article

- The Medicare Initial Enrollment Period Is 7 Months Total

- Why People Call It the 3-Month Medicare Window

- The Biggest Mistake: Thinking Medicare Starts Automatically

- Part A May Start Automatically, But Part B Is Different

- Why the 3 Months Before Your Birthday Matter Most

- If You Are Still Working, Talk to HR

- Do Not Confuse Medicare With Social Security

- What Happens If You Wait Too Long?

- Medicare Advantage, Part D, and Supplement Choices Come Next

- A Typical Example

- What You Should Do Before You Turn 65

- My Opinion After Years of Helping People With Medicare

- The Bottom Line

A lot of people ask, “What is the Medicare 3-month enrollment window?”

That is a very good question, but here is the important thing to understand right away:

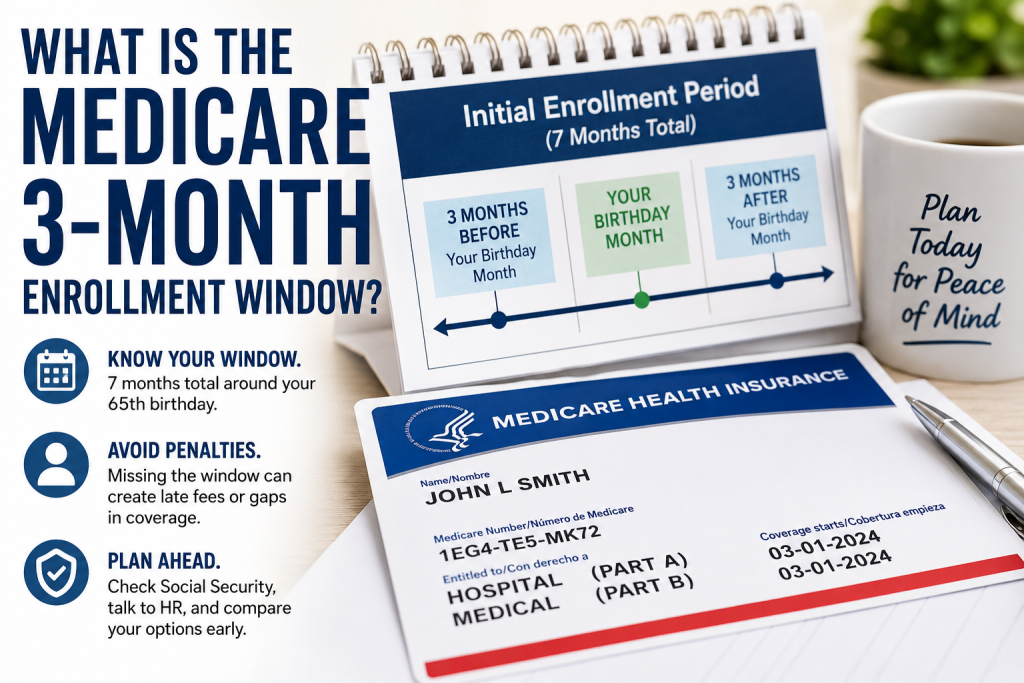

Your first Medicare enrollment period is usually not just 3 months. It is normally 7 months total.

The confusion comes from the fact that Medicare’s Initial Enrollment Period includes:

- 3 months before the month you turn 65

- The month you turn 65

- 3 months after the month you turn 65

So when people talk about the “Medicare 3-month enrollment window,” they are usually talking about one part of the larger 7-month window.

And this matters.

Because if you misunderstand the window, you may wait too long, miss an important deadline, or end up with a gap in coverage.

After helping people with Medicare for many years, I can tell you this: one of the biggest mistakes people make is assuming Medicare will simply start automatically when they turn 65.

Sometimes it does.

Sometimes it does not.

And that little “sometimes” is where the trouble begins.

The Medicare Initial Enrollment Period Is 7 Months Total

Your Medicare Initial Enrollment Period is your first opportunity to sign up for Medicare when you become eligible at age 65.

It is 7 months long.

It starts 3 months before the month you turn 65 and ends 3 months after the month you turn 65.

For example, if your birthday is in June, your Initial Enrollment Period would generally include:

- March

- April

- May

- June

- July

- August

- September

That is the full 7-month window.

So the better way to explain it is this:

There is not one single 3-month Medicare enrollment window. There is a 7-month Initial Enrollment Period that includes two important 3-month periods: before your birthday month and after your birthday month.

That may sound like a small difference, but in Medicare, small misunderstandings can become expensive.

Why People Call It the 3-Month Medicare Window

People often focus on the 3 months before turning 65 because that is usually the best time to get ready.

That is when you should start asking the important questions:

- Do I need to sign up for Medicare?

- Will I be enrolled automatically?

- Do I need Medicare Part B?

- Am I still working?

- Do I have employer coverage?

- Do I need a prescription drug plan?

- Should I compare Medicare Advantage plans?

- Should I look at a Medicare Supplement?

The 3 months before your birthday month are very important because they give you time to make decisions before you are in a rush.

The 3 months after your birthday month are also part of the Initial Enrollment Period, but I do not like seniors treating that as a reason to wait.

Yes, you may still have time after your birthday month.

But waiting can affect when your coverage starts.

And if there is one thing you do not want with Medicare, it is finding out too late that you misunderstood the timing.

The Biggest Mistake: Thinking Medicare Starts Automatically

The most common mistake I see is simple:

People think Medicare starts automatically.

They assume that because the government knows their birthday, Medicare will just show up.

And sometimes, that is partly true.

But not always.

This is where people get confused.

Some people are automatically enrolled in Medicare because they are already receiving Social Security benefits before age 65.

But other people are not receiving Social Security yet. They may still be working. They may have delayed Social Security. They may assume everything is automatic when it is not.

That is why my advice is simple:

Do not assume Medicare will start automatically.

Verify it.

That one step can save you a lot of aggravation.

Part A May Start Automatically, But Part B Is Different

One of the most important things seniors need to understand is the difference between Medicare Part A and Medicare Part B.

Medicare Part A is hospital insurance.

For many people, Part A does not have a monthly premium because they or their spouse paid Medicare taxes while working.

Medicare Part B is medical insurance.

Part B helps cover doctor visits, outpatient care, preventive services, and other medical services.

Part B usually has a monthly premium.

This is where people get tripped up.

Part A may start automatically for some people.

But Part B may require action.

And because Part B has a monthly premium, how that premium is paid also matters.

If you are receiving Social Security, your Part B premium may be taken directly out of your Social Security payment.

But if you are not receiving Social Security yet, you may have to pay the Part B premium another way, usually by getting a bill.

That surprises people.

They think, “I have Medicare,” but they may not fully understand whether they have Part A only, whether they have Part B, or whether the Part B premium is being paid correctly.

That is not a tiny detail.

That can affect your coverage, your doctor visits, your ability to enroll in certain plans, and whether you end up with problems later.

Why the 3 Months Before Your Birthday Matter Most

In my opinion, the most important part of the Medicare enrollment window is the 3 months before your birthday month.

That is the time to get serious.

Not panicked.

Not pressured.

Just serious.

This is when you should check your situation and find out what applies to you.

The biggest mistake is waiting until after your birthday and then trying to figure everything out in a hurry.

Medicare is not like ordering a pair of socks online.

You do not want to click the wrong thing, miss the wrong deadline, or misunderstand the wrong letter.

The 3 months before your birthday month give you time to slow down and make better decisions.

If You Are Still Working, Talk to HR

If you are still working when you turn 65, or if you are covered by a spouse’s employer plan, do not guess.

Talk to HR.

This is very important.

Ask them how your employer coverage works with Medicare.

Ask whether you need to sign up for Part B now.

Ask whether your prescription drug coverage is considered creditable.

Ask what happens when you retire or leave the employer plan.

This matters because Medicare rules can depend on your employer coverage, the size of the employer, and whether the coverage is based on current employment.

One person may need Part B at 65.

Another person may be able to delay Part B because they have qualifying employer coverage.

That is why you should not make your Medicare decision based on what your neighbor did.

Your neighbor may be a wonderful person.

Your neighbor may also be completely wrong for your situation.

Do Not Confuse Medicare With Social Security

Another common misunderstanding is confusing Medicare with Social Security.

They are connected, but they are not the same thing.

Social Security handles enrollment for Medicare Part A and Part B.

But deciding when to take Social Security and deciding when to enroll in Medicare are two different decisions.

Some people take Social Security before 65.

Some people delay Social Security.

Some people keep working.

Some people retire early.

Some people have employer coverage.

All of these situations can affect what they need to do with Medicare.

That is why “Medicare starts automatically” is not a safe statement unless you know the person’s exact situation.

What Happens If You Wait Too Long?

If you wait too long or miss the correct Medicare enrollment window, you may create problems for yourself.

Depending on your situation, you could face:

- A gap in coverage

- A delay in when coverage starts

- A late enrollment penalty

- Problems enrolling in Part B

- Problems with prescription drug coverage

- Confusion when trying to choose a Medicare Advantage or Supplement plan

This is the part I want seniors to take seriously.

Missing the window can create penalties or gaps in coverage.

And the frustrating part is that many of these problems can be avoided by checking early.

Not guessing.

Not assuming.

Checking.

Medicare Advantage, Part D, and Supplement Choices Come Next

Signing up for Medicare Part A and Part B is only the beginning.

After that, you may need to decide how you want to receive your Medicare coverage.

You may want to compare:

- Medicare Advantage plans

- Medicare Supplement plans

- Medicare Part D prescription drug plans

- Doctor networks

- Drug coverage

- Dental, vision, and hearing benefits

- Monthly premiums

- Maximum out-of-pocket costs

- Travel coverage

- Referral rules

- Pharmacy choices

This is where many people feel overwhelmed.

They thought the question was, “When do I sign up for Medicare?”

Then they discover the next question is, “What kind of Medicare coverage should I choose?”

That is why I believe people should start early.

Not because they should be rushed into a plan.

Not because they should let someone pressure them.

But because they deserve time to compare their choices privately and calmly.

A Typical Example

Here is a common situation.

Someone is turning 65.

They are not taking Social Security yet.

They assume Medicare will start automatically.

They wait.

Then they find out that Medicare Part A may not be the whole story. They may still need to sign up for Part B. They may need to pay the Part B premium directly because they are not yet receiving Social Security. They may also need to think about drug coverage.

Now they are rushing.

Now they are confused.

Now they are trying to fix something that could have been handled earlier.

That is why the 3 months before your birthday month matter so much.

That is your planning window.

Use it.

What You Should Do Before You Turn 65

Before your 65th birthday, take these steps.

Check with Social Security.

Find out whether you will be automatically enrolled in Medicare or whether you need to sign up.

Talk to HR if you are still working.

Ask whether your employer coverage works with Medicare and whether you need Part B.

Confirm your Part B situation.

Do not assume you have Part B. Do not assume you do not need it. Confirm it.

Look at Part D prescription drug coverage.

Even if you do not take many medications now, you still need to understand the rules.

Compare Medicare Advantage and Medicare Supplement options early.

These are different choices with different costs, rules, benefits, and networks.

Do not wait until the last minute.

Medicare is easier when you are not under pressure.

My Opinion After Years of Helping People With Medicare

My honest opinion is that Medicare is more confusing than it needs to be.

Most seniors are not asking for a college course in Medicare.

They want plain answers.

They want to know:

- What do I need to do?

- When do I need to do it?

- What happens if I miss it?

- Do I need Part B?

- Can I keep my doctor?

- Do I need drug coverage?

- What is the safest next step?

That is not too much to ask.

But instead, many people get flooded with mail, phone calls, commercials, and confusing terms.

It becomes a Medicare media circus.

And in the middle of all that noise, the most important thing can get lost:

You need to know your enrollment window.

The Bottom Line

So, is the Medicare enrollment window 3 months or 7 months?

The correct answer is:

Medicare’s Initial Enrollment Period is usually 7 months total.

It includes the 3 months before your birthday month, your birthday month, and the 3 months after your birthday month.

The reason people call it the “3-month window” is because they are usually referring to one part of that larger 7-month period.

But do not let the wording confuse you.

The safest time to start is during the 3 months before your birthday month.

That gives you time to check Social Security, talk to HR if you are still working, confirm whether you need Part B, look at Part D, and compare Medicare Advantage or Medicare Supplement options.

The most dangerous thing you can do is assume everything will happen automatically.

Sometimes Part A may start automatically.

Sometimes Part B requires action.

Sometimes the premium comes out of Social Security.

Sometimes you may have to pay it directly.

So here is the message I want you to remember:

Missing the window can create penalties or gaps in coverage.

Do not assume.

Verify.

Medicare does not have to be scary.

But it does have to be handled.

William Vargas brings over 50 years of financial and insurance expertise to every Medicare conversation. He operates MedicareSelfEnroll.com, helping seniors in Florida, New York, and North Carolina — with no pressure, no phone calls required.