In This Article

- Medicare Advantage vs. Medigap: Two Very Different Ways to Handle Medicare

- What Is Original Medicare?

- What Is Medicare Advantage?

- What Is Medigap?

- The Biggest Difference: Network vs. Freedom of Choice

- The Cost Difference

- Prescription Drug Coverage

- Extra Benefits: Dental, Vision, Hearing, and More

- Can You Have Medicare Advantage and Medigap Together?

- Which One Is Better?

- The Annual Review Problem

- A Simple Everyday Example

- Questions to Ask Before Choosing

- Final Takeaway

- FAQ: Medicare Advantage vs. Medigap

Medicare Advantage vs. Medigap: Two Very Different Ways to Handle Medicare

When people first enter Medicare, one of the most confusing decisions is this:

Should I choose Medicare Advantage or Medigap?

And right away, let’s clear up the biggest misunderstanding.

Medicare Advantage and Medigap are not the same thing.

They are not two names for the same product. They do not work the same way. And in most cases, you do not use them together.

Think of it this way:

Medicare Advantage is a different way to receive your Medicare benefits through a private insurance plan approved by Medicare.

Medigap, also called Medicare Supplement Insurance, is extra insurance you buy to help pay some of the out-of-pocket costs left behind by Original Medicare.

That may sound simple, but the real difference shows up when you go to the doctor, need a specialist, travel, get prescriptions, or face a serious illness. That is where the rubber meets the road — or, in Medicare language, where the bill meets the kitchen table.

What Is Original Medicare?

Before comparing Medicare Advantage and Medigap, you need to understand the starting point: Original Medicare.

Original Medicare includes:

Medicare Part A, which helps cover hospital care, skilled nursing facility care, hospice care, and some home health care.

Medicare Part B, which helps cover doctor visits, outpatient care, preventive services, medical equipment, and many medically necessary services.

Original Medicare is run by the federal government. You can generally see any doctor or hospital in the United States that accepts Medicare. However, Original Medicare does not pay 100% of everything. You may still owe deductibles, coinsurance, and copayments.

That is why many people look at either Medicare Advantage or Medigap.

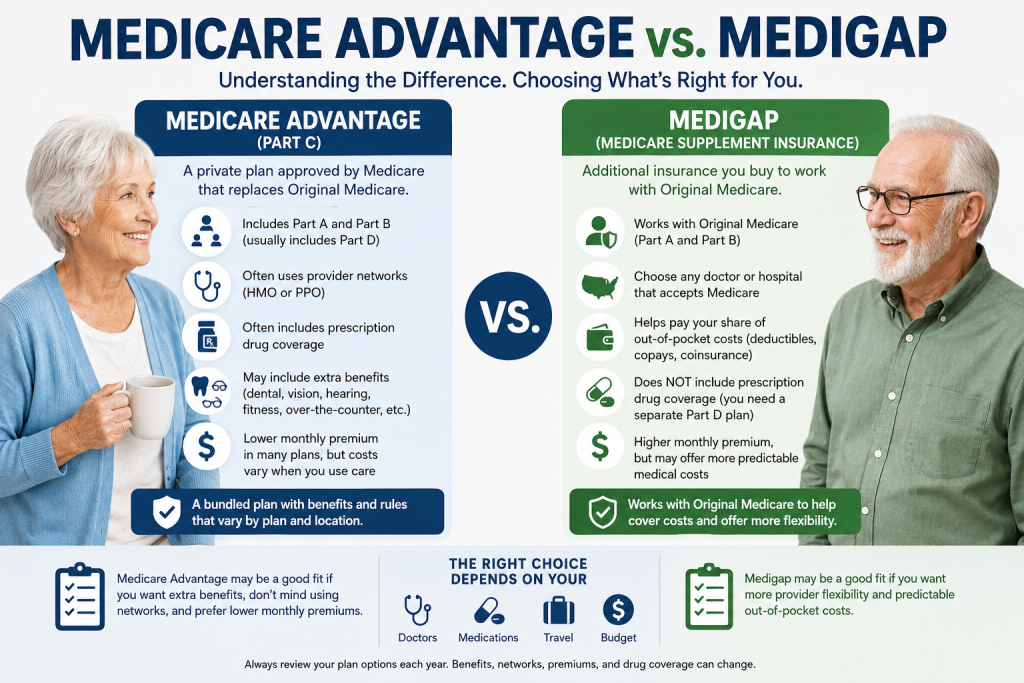

What Is Medicare Advantage?

Medicare Advantage is also called Medicare Part C. It is offered by private insurance companies that are approved by Medicare. Medicare Advantage plans provide your Part A and Part B benefits, and many plans also include Part D prescription drug coverage. Medicare explains that Medicare Advantage plans are an alternative to Original Medicare and often bundle Part A, Part B, and usually Part D into one plan.

Many Medicare Advantage plans may also offer extra benefits that Original Medicare does not usually cover, such as dental, vision, hearing, fitness benefits, transportation, over-the-counter allowances, or wellness programs. These benefits vary by plan, county, and year.

That last part is important: Medicare Advantage plans are local.

A plan available in one county may not be available in the next county. The doctors, hospitals, drug coverage, copays, and extra benefits can change from one plan to another.

So Medicare Advantage can be attractive, especially when the premium is low and extra benefits are included. But you must look carefully at the details.

What Is Medigap?

Medigap is also called Medicare Supplement Insurance. It is private insurance that works with Original Medicare.

Medigap helps pay your share of certain out-of-pocket costs in Original Medicare, such as copayments, coinsurance, and deductibles. Medicare states that you generally must have both Part A and Part B to buy a Medigap policy.

Here is how it works:

You go to a doctor who accepts Medicare. Medicare pays its approved share. Then your Medigap policy may help pay some or all of the remaining amount, depending on which Medigap plan you have. Medicare explains that with most Medigap policies, Medicare pays first, and then the Medigap policy pays according to its benefits.

Medigap does not replace Original Medicare. It sits beside it.

That is the biggest difference from Medicare Advantage.

With Medigap, you are still using Original Medicare as your main coverage. With Medicare Advantage, you are receiving your Medicare benefits through the Medicare Advantage plan.

The Biggest Difference: Network vs. Freedom of Choice

This is one of the most important practical differences.

With Original Medicare plus Medigap, you can generally see any doctor or hospital in the United States that accepts Medicare. You usually do not have to stay inside a local network.

With Medicare Advantage, many plans use provider networks. Some are HMOs, some are PPOs, and each plan has its own rules. You may need to use in-network doctors and hospitals to get the lowest costs. Some plans may require referrals for specialists.

This does not mean Medicare Advantage is bad. It means you need to check carefully.

If your doctors, hospital, specialists, and medications fit well inside a Medicare Advantage plan, it may work very nicely.

But if you travel often, split time between states, see several specialists, or want broad provider flexibility, Medigap may feel more comfortable.

Medicare itself tells beneficiaries to consider doctor and hospital choice, cost, coverage, and travel when comparing Original Medicare and Medicare Advantage.

The Cost Difference

This is where many people get confused.

Medicare Advantage plans often have low monthly premiums. Some plans may even have a $0 plan premium, although you still must continue paying your Medicare Part B premium.

But low premium does not mean no cost.

With Medicare Advantage, you may pay copays or coinsurance when you use care. You may pay for doctor visits, specialists, hospital stays, scans, outpatient surgery, urgent care, and other services depending on the plan.

Medicare Advantage plans also have an annual out-of-pocket maximum for covered Part A and Part B services. That can protect you from unlimited medical costs, but the limit can still be several thousand dollars.

With Medigap, you usually pay a separate monthly premium for the Medigap policy. That premium may be higher than a Medicare Advantage plan premium. But in return, your medical costs may be more predictable, depending on the Medigap plan you choose.

So the tradeoff is simple:

Medicare Advantage may cost less each month but may cost more when you use care.

Medigap may cost more each month but may reduce surprise medical bills.

It is like choosing between paying less up front or paying more for predictability. Neither answer is perfect for everyone.

Prescription Drug Coverage

This is another major difference.

Many Medicare Advantage plans include prescription drug coverage. These are often called MA-PD plans, meaning Medicare Advantage Prescription Drug plans.

Medigap does not include prescription drug coverage. If you choose Original Medicare plus Medigap and want drug coverage, you generally need to buy a separate Medicare Part D prescription drug plan.

That means with Medigap, your package may look like this:

Original Medicare Part A

Original Medicare Part B

Medigap policy

Separate Part D drug plan

With Medicare Advantage, your package may look like this:

One Medicare Advantage plan that includes hospital, medical, and usually drug coverage.

That bundled structure is one reason Medicare Advantage appeals to many people. But again, the drug list, pharmacy network, copays, and prior authorization rules matter. You cannot just look at the dental benefit and call it a day. That is like buying a car because the cup holder is nice.

Extra Benefits: Dental, Vision, Hearing, and More

Medicare Advantage plans may include extra benefits that Original Medicare does not usually cover, such as routine dental, vision, hearing, fitness memberships, transportation, and over-the-counter benefits. Medicare notes that Medicare Advantage plans may offer extra benefits that Original Medicare does not cover.

This is one of the biggest selling points of Medicare Advantage.

Many seniors like having dental, vision, and hearing benefits included. And honestly, who would not want help with dental bills? A crown can cost enough to make you think the dentist is installing a chandelier in your mouth.

But you still need to read the details.

Some dental benefits are generous. Some are limited. Some have networks. Some cover cleanings but not major work. Some advertise a large dollar amount, but the rules may limit how useful it really is.

Medigap usually does not include dental, vision, or hearing benefits. It is mainly designed to help with the medical cost-sharing left over from Original Medicare.

So the question becomes:

Do you want extra benefits bundled into one plan?

Or do you want broader medical flexibility and predictable medical cost-sharing?

That is the real decision.

Can You Have Medicare Advantage and Medigap Together?

In most situations, no.

Medigap is designed to work with Original Medicare, not Medicare Advantage.

If you enroll in a Medicare Advantage plan, a Medigap policy generally cannot pay your Medicare Advantage copays, deductibles, or coinsurance.

This is a critical point because many people hear “supplement” and think they can add it to anything. But Medigap supplements Original Medicare. It does not supplement Medicare Advantage.

So when you choose, you are generally choosing one road:

Road 1: Original Medicare + Medigap + Part D

Road 2: Medicare Advantage, usually with drug coverage included

You do not drive both cars at the same time. At least not unless you want the insurance equivalent of a fender bender.

Which One Is Better?

The honest answer is: it depends on your situation.

Anyone who says one is always better is selling you something — or has not looked closely enough.

Medicare Advantage may be a better fit if:

You want a lower monthly premium.

You are comfortable using a provider network.

Your doctors and hospitals are in the plan.

Your prescriptions are covered well.

You like having dental, vision, hearing, and extra benefits bundled.

You do not travel much outside your service area for care.

You are willing to review your plan every year.

Medigap may be a better fit if:

You want broad access to Medicare-accepting providers nationwide.

You travel often or live in more than one state during the year.

You want more predictable medical costs.

You do not want to worry as much about networks.

You are willing to pay a separate monthly premium.

You are comfortable adding a separate Part D prescription drug plan.

The “better” choice depends on your doctors, medications, budget, travel, health conditions, and how much risk you are comfortable carrying.

The Annual Review Problem

Medicare Advantage plans can change each year. Premiums, copays, drug formularies, provider networks, dental benefits, and other details may change.

Part D drug plans can also change each year.

That is why Medicare beneficiaries should review coverage during the Annual Enrollment Period, even if they are happy with their current plan.

Medigap benefits are standardized by plan letter in most states. Medicare says Medigap policies are standardized and named by letters, such as Plan G or Plan K, and the benefits in each lettered plan are the same no matter which insurance company sells it.

That does not mean Medigap premiums stay the same. Premiums can increase. But the structure of the benefits is generally more stable than Medicare Advantage plan benefits.

A Simple Everyday Example

Let’s say Mary is 67, lives in one county year-round, has doctors she likes, takes a few prescriptions, and finds a Medicare Advantage plan where her doctors, hospital, and drugs are all covered well. She likes the dental and vision benefits. She may be happy with Medicare Advantage.

Now let’s say Robert is 72, travels between New York and Florida, sees specialists in different states, and wants the freedom to see any provider who accepts Medicare. He does not want to worry about local networks. He may prefer Original Medicare plus Medigap and a Part D plan.

Same Medicare system. Different lives. Different answers.

That is why the right question is not, “Which plan is best?”

The right question is:

Which option fits the way I actually live?

Questions to Ask Before Choosing

Before choosing Medicare Advantage or Medigap, ask yourself:

Are my doctors in the plan?

Are my hospitals in the plan?

Are my prescriptions covered?

What are the copays for specialists and hospital care?

What is the annual out-of-pocket maximum?

Do I travel often?

Do I want dental, vision, and hearing benefits included?

Can I afford a higher monthly premium for more predictable medical costs?

Am I comfortable reviewing my plan every year?

Do I understand what happens if I want to switch later?

That last question matters. In many states, switching from Medicare Advantage back to Original Medicare and then getting Medigap later may require medical underwriting, depending on timing and state rules. That means you may not always be guaranteed the Medigap policy you want later. This is one reason people should not make the first decision casually.

Medicare is not a place for guessing. Guessing is fine when choosing soup. It is not fine when choosing health coverage.

Final Takeaway

Medicare Advantage and Medigap are two different paths.

Medicare Advantage is usually a bundled private plan that replaces the way you receive Original Medicare benefits. It may include drug coverage and extra benefits, but it often comes with networks, copays, and plan rules.

Medigap works with Original Medicare and helps pay some of the costs Medicare leaves behind. It usually offers broader provider flexibility, but you pay a separate premium and usually need a separate Part D drug plan.

The best choice is not the one with the flashiest brochure. The best choice is the one that fits your doctors, prescriptions, budget, travel habits, and comfort level.

In plain English:

Medicare Advantage may offer convenience and extras.

Medigap may offer flexibility and predictability.

Both can be good. Both can be wrong. The trick is knowing which one is right for you before you enroll.

FAQ: Medicare Advantage vs. Medigap

Is Medigap the same as Medicare Advantage?

No. Medicare Advantage is an alternative way to receive Medicare benefits through a private plan. Medigap is supplemental insurance that works with Original Medicare.

Can I have both Medicare Advantage and Medigap?

Generally, no. Medigap is designed to work with Original Medicare, not Medicare Advantage.

Does Medicare Advantage include prescription drugs?

Many Medicare Advantage plans include Part D prescription drug coverage, but not all. You must check the plan details.

Does Medigap include prescription drugs?

No. If you choose Medigap and want prescription drug coverage, you usually need a separate Part D plan.

Which has better doctor choice?

Original Medicare plus Medigap generally offers broader access to doctors and hospitals that accept Medicare. Medicare Advantage plans may use networks.

Which costs less?

Medicare Advantage may have lower monthly premiums, but you may pay copays and coinsurance when you use care. Medigap usually has a separate monthly premium but may make medical costs more predictable.

Is Medicare Advantage bad?

No. Medicare Advantage can work well for many people. The issue is whether the specific plan fits your doctors, prescriptions, budget, and health needs.

Is Medigap better for travelers?

Often, yes. Because Original Medicare is accepted nationwide by providers who take Medicare, Medigap may be more comfortable for people who travel frequently or live in more than one state.

William Vargas brings over 50 years of financial and insurance expertise to every Medicare conversation. He operates MedicareSelfEnroll.com, helping seniors in Florida, New York, and North Carolina — with no pressure, no phone calls required.