In This Article

- What Are Out-of-Pocket Costs?

- “Covered” Does Not Mean “Free”

- Start With What Kind of Medicare You Have

- Drug Costs Are a Separate Issue

- Ask for a Cost Estimate Before Treatment

- Call Your Plan With the Exact Information

- Watch Out for Separate Bills

- Cancer Treatment Requires Extra Cost Questions

- Prior Authorization Can Affect Costs

- In Network vs. Out of Network

- Use Your Plan Documents

- Use Medicare.gov and Your Plan Website

- Ask About Payment Options

- Do Not Wait Until the Bill Arrives

- A Simple Checklist Before Major Care

- The Bottom Line

One of the most frustrating phrases in health care is: “It’s covered.”

That sounds reassuring, but it does not always answer the real question.

The real question is: “How much will I personally have to pay?”

That is your out-of-pocket cost. And for seniors, especially those on Medicare, that number matters. A treatment may be covered by Medicare, a Medicare Advantage plan, or a Part D drug plan, but that does not automatically mean it will cost you nothing.

Covered means the insurance company or Medicare recognizes the service as eligible for payment. It does not always mean fully paid.

That is where people get surprised. And in health care, surprises are usually expensive.

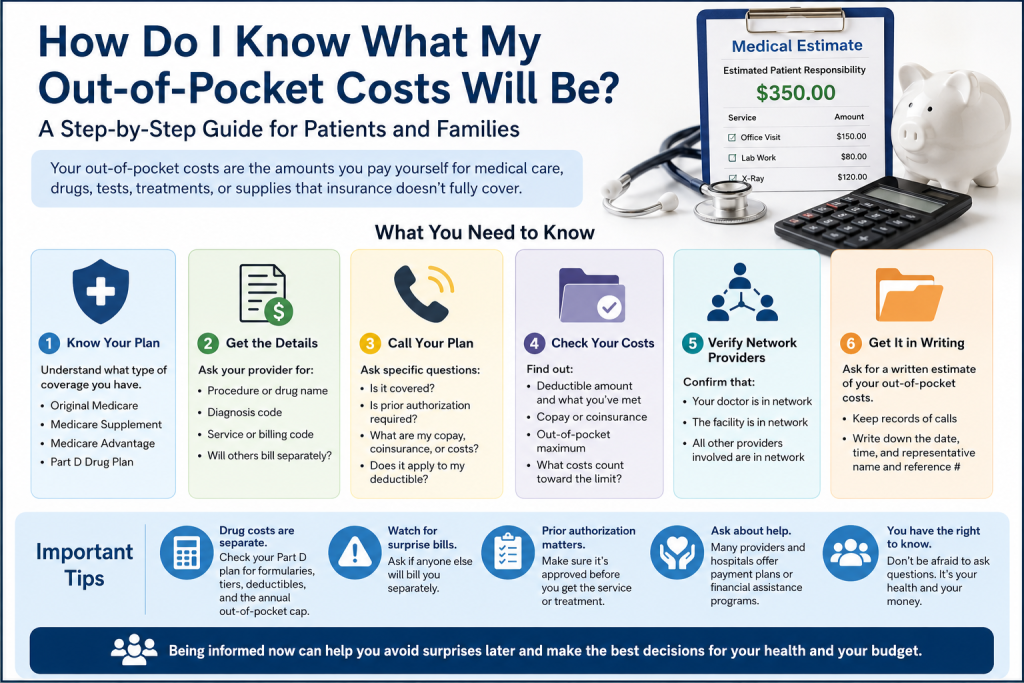

What Are Out-of-Pocket Costs?

Out-of-pocket costs are the amounts you pay yourself for medical care, drugs, tests, treatments, hospital stays, or supplies that insurance does not fully cover.

These can include:

Premiums

Deductibles

Copayments

Coinsurance

Drug costs

Out-of-network charges

Non-covered services

Transportation or travel costs

Caregiver costs

Follow-up visits

Medical equipment

The National Cancer Institute uses the term financial toxicity to describe the financial stress caused by medical treatment costs. This is especially common in cancer care, where treatment can involve specialists, imaging, drugs, hospital visits, and repeated follow-ups. Out-of-pocket costs are the part of medical care that your insurance does not pay.

That is a serious issue. A person can be medically treated and financially wounded at the same time. Nobody wants that.

“Covered” Does Not Mean “Free”

This is the first rule.

When your doctor says, “Medicare covers this,” that is only the beginning of the conversation.

You need to ask:

What part of Medicare covers it?

Is it covered under Part A, Part B, Part C, or Part D?

Does my plan require prior authorization?

Is the doctor in network?

Is the facility in network?

Is the drug on my plan’s formulary?

What tier is the drug on?

Is there a deductible?

Is there coinsurance?

This may sound like a lot, but it is better to ask these questions before treatment than to stare at a bill later like it just fell out of the sky.

Start With What Kind of Medicare You Have

Your out-of-pocket costs depend heavily on what type of Medicare coverage you have.

There are three common situations.

1. Original Medicare Only

Original Medicare includes Part A for hospital care and Part B for doctor and outpatient services.

With Original Medicare, after the Part B deductible, you usually pay 20% of the Medicare-approved amount for many covered services. For 2026, the standard Medicare Part B premium is $202.90 per month, and the annual Part B deductible is $283.

That 20% can be manageable for a small office visit. But for expensive treatment, imaging, chemotherapy, infusions, or medical equipment, 20% can become a very large number.

Also, Original Medicare by itself does not have the same kind of annual out-of-pocket maximum that Medicare Advantage plans have. That is why many people with Original Medicare also buy a Medicare Supplement, also called Medigap.

2. Original Medicare Plus a Medicare Supplement

A Medicare Supplement helps pay some of the costs that Original Medicare does not pay, such as deductibles, coinsurance, and copayments.

This can make costs more predictable, but you still need to know:

Which Medigap plan you have

Whether Medicare covers the service

Whether the provider accepts Medicare assignment

Whether the service is medically necessary

Whether a drug is covered under Part B or Part D

A Medicare Supplement does not turn every medical expense into zero. But it can reduce uncertainty.

3. Medicare Advantage

Medicare Advantage plans are private plans approved by Medicare. These plans usually have networks, copays, coinsurance, prior authorization rules, and an annual maximum out-of-pocket limit for covered medical services.

For 2026, the federal maximum out-of-pocket limit for Medicare Advantage in-network covered services is $9,250, although many plans may set lower limits.

That number is important. It means there is a ceiling on covered in-network medical costs, but it does not mean everything counts toward that ceiling.

For example, Part D drug costs generally do not count toward the Medicare Advantage medical maximum out-of-pocket limit. You must look at your plan’s Evidence of Coverage to see exactly what counts and what does not.

Drug Costs Are a Separate Issue

Prescription drugs can be one of the biggest surprises.

A drug may be covered, but your cost depends on:

Whether it is covered under Part B or Part D

Whether it is on the formulary

Which tier it is on

Whether prior authorization is required

Whether step therapy is required

Whether there is a deductible

Whether it is a specialty drug

Whether there is coinsurance instead of a flat copay

For Medicare Part D, covered drug costs have an annual out-of-pocket cap. In 2026, Medicare Part D out-of-pocket costs for covered drugs are capped at $2,100. After reaching that limit, you do not pay copays or coinsurance for covered Part D drugs for the rest of the calendar year.

That is good news, but there is a catch: the drug must be covered by your plan.

A drug that is not on the formulary, or not approved by the plan, may still create problems. That is why you must check the drug specifically by name, dosage, pharmacy, and plan.

Ask for a Cost Estimate Before Treatment

Before a major test, surgery, infusion, cancer treatment, or expensive drug, ask for a written estimate.

Do not be shy. You are not being difficult. You are being responsible.

Ask the provider’s billing office:

Can you give me the procedure code or billing code?

What diagnosis code will be used?

Is this provider in network?

Is this facility in network?

Will any outside lab, anesthesiologist, radiologist, or specialist bill separately?

Has prior authorization been approved?

What is my estimated responsibility?

That last question is the big one: What is my estimated responsibility?

You want the estimate before the service, not after the bill arrives.

Call Your Plan With the Exact Information

Once you have the provider name, facility name, drug name, and procedure codes, call your insurance plan.

Ask:

Is this service covered under my plan?

Is prior authorization required?

Has it been approved?

Is the doctor in network?

Is the facility in network?

What will my copay or coinsurance be?

Does this apply to my deductible?

How much of my deductible have I already met?

How much have I paid toward my maximum out-of-pocket limit?

Does this cost count toward that limit?

And here is a very important tip: write down the date, time, representative’s name, and reference number for the call.

Insurance conversations have a way of disappearing into the fog. Get a reference number.

Watch Out for Separate Bills

Many people think they are getting one service from one provider. Then the bills start arriving from every direction.

For example, a hospital procedure may involve:

The surgeon

The hospital

The anesthesiologist

The lab

The radiologist

The pathology department

The imaging center

The pharmacy

Medical equipment suppliers

You may think you went to one place for one procedure. The billing system may see seven different billers with seven different charges.

That is why you should ask ahead of time: Who else will bill me?

This is especially important with hospitals, outpatient surgical centers, cancer centers, and emergency care.

Cancer Treatment Requires Extra Cost Questions

Cancer care can be especially complicated because treatment may include surgery, radiation, chemotherapy, immunotherapy, targeted drugs, genetic testing, scans, lab work, and follow-up care.

The National Cancer Institute notes that cancer patients and survivors are more likely to experience financial toxicity than people without cancer. Costs can affect not only medical bills, but also work, household finances, and family stress.

So when discussing cancer treatment, ask the oncology office:

Is there a financial counselor I can speak with?

Is this drug covered by Medicare Part B or Part D?

Is there a patient assistance program?

Are there lower-cost treatment alternatives?

Is biomarker testing covered?

Will this treatment require repeated scans or lab work?

Will I need transportation help?

Are there foundation grants or copay assistance programs?

This is not begging. This is part of modern medical care. A treatment plan should include a financial plan.

Prior Authorization Can Affect Costs

Prior authorization means the insurance company must approve the service before it is performed.

If prior authorization is required and not approved, you could face a denial. That does not always mean you owe the full bill, but it can create delays, appeals, confusion, and stress.

Before treatment, ask both the provider and the plan:

Is prior authorization required?

Was it submitted?

Was it approved?

What date was it approved?

What exactly was approved?

How long is the authorization valid?

Do not accept vague answers like, “We usually take care of that.”

Usually is not good enough. You want confirmation.

In Network vs. Out of Network

If you have Medicare Advantage, network status matters a lot.

Your doctor may be in network, but the hospital may not be. The facility may be in network, but one specialist involved may not be. That is where people get blindsided.

Ask separately:

Is my doctor in network?

Is the hospital or facility in network?

Are all other providers involved in network?

What happens if someone out of network is used?

With Original Medicare, the key question is usually whether the provider accepts Medicare assignment. That means the provider agrees to accept the Medicare-approved amount as full payment.

Use Your Plan Documents

Every Medicare Advantage and Part D plan has documents that explain costs.

The most important are:

Evidence of Coverage

Summary of Benefits

Drug Formulary

Annual Notice of Change

Provider Directory

Pharmacy Directory

The Evidence of Coverage is not exactly light bedtime reading. It has all the charm of a toaster manual written by lawyers. But it is important.

That document explains copays, coinsurance, deductibles, maximum out-of-pocket limits, prior authorization rules, and what services are covered.

Use Medicare.gov and Your Plan Website

Medicare.gov can help you compare plans, drug costs, pharmacies, and coverage options. Your private plan website may also show claims, deductibles, authorizations, provider network information, and drug pricing.

But do not rely only on websites for expensive care. Websites can be outdated or incomplete.

For major costs, confirm by phone and keep records.

Ask About Payment Options

If the cost is high, ask about payment arrangements before the bill becomes a crisis.

Ask:

Do you offer payment plans?

Is there financial assistance?

Do you have charity care?

Can I speak with a billing specialist?

Is there a social worker or patient navigator?

Are there grants or foundations for my condition?

Hospitals, cancer centers, and large medical groups often have financial assistance policies. But many patients never ask, so they never find out.

Do Not Wait Until the Bill Arrives

The worst time to figure out your out-of-pocket cost is after the treatment.

By then, you are tired, worried, and holding a bill that looks like it was printed by a slot machine.

Before treatment, slow the process down enough to ask questions.

You have the right to understand the financial side of your care.

A Simple Checklist Before Major Care

Before surgery, cancer treatment, expensive imaging, specialty drugs, or hospital care, go through this checklist:

- What is the exact service, drug, or procedure?

- What billing codes will be used?

- Is the provider in network?

- Is the facility in network?

- Is prior authorization required?

- Has authorization been approved?

- What is my deductible?

- How much of my deductible have I met?

- What is my copay or coinsurance?

- Does this count toward my maximum out-of-pocket limit?

- Will anyone else bill me separately?

- Is there a lower-cost alternative?

- Is financial assistance available?

- Can I get the estimate in writing?

- Can I get a reference number from my insurance plan?

That checklist may save you money, stress, and a lot of aggravation.

The Bottom Line

To know your out-of-pocket costs, you need more than the word “covered.”

You need to know how it is covered, who is billing, what your plan rules are, whether authorization is required, and what your share will be.

The best approach is simple:

Get the exact treatment information.

Ask the provider for an estimate.

Call your plan.

Confirm network status.

Confirm prior authorization.

Ask what counts toward your deductible and out-of-pocket maximum.

Write everything down.

Modern medicine is advancing quickly. That is good news. But modern medical billing can still feel like a maze with no exit sign.

So do not be embarrassed to ask questions. Do not assume. Do not wait for the bill.

Because in health care, one of the smartest things you can say is:

“Before we do this, what will it cost me?”

William Vargas brings over 50 years of financial and insurance expertise to every Medicare conversation. He operates MedicareSelfEnroll.com, helping seniors in Florida, New York, and North Carolina — with no pressure, no phone calls required.