In This Article

- The First Path: Original Medicare

- The Second Path: Medicare Advantage

- The Question Is Not “Which One Is Better?”

- Compare Your Doctors First

- Compare Your Prescriptions Next

- Compare the Full Yearly Cost

- Watch the Extra Benefits

- Travel Matters More Than People Think

- Why Self-Enroll Gives Seniors More Control

- The Simple Medicare Decision Checklist

- Final Thoughts

- Is Medicare Advantage the same as Original Medicare?

- Does Original Medicare require prior authorization?

- Do Medicare Advantage plans include prescription drug coverage?

- What is the 2026 Medicare Part D out-of-pocket cap?

- What is the maximum Part D deductible in 2026?

- What is the Medicare Part B deductible in 2026?

- Is Medicare Advantage better than Original Medicare?

- Can I compare Medicare plans online?

- Is MedicareSelfEnroll.com affiliated with Medicare?

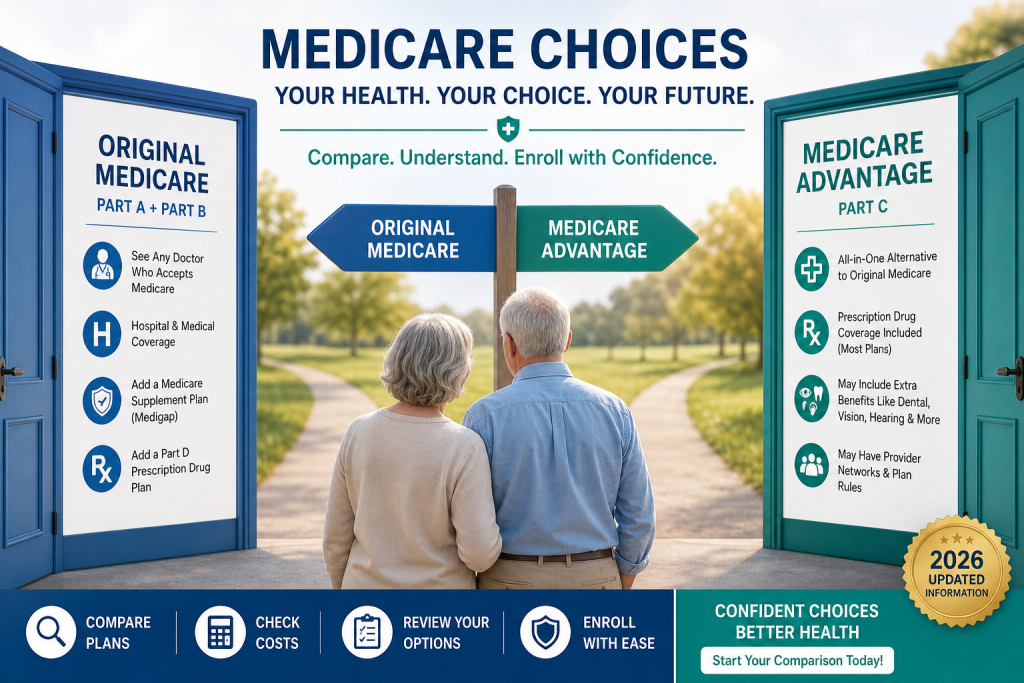

Choosing Medicare coverage can feel like standing in front of two doors.

Behind one door is Original Medicare.

Behind the other is Medicare Advantage.

Both can work. Both can protect you. Both can be the right choice for the right person.

But they are not the same.

And in 2026, seniors should understand the difference before choosing a plan, because the wrong fit can lead to frustration, higher costs, limited access to doctors, or surprise rules you did not expect.

Medicare is too important to choose by guessing.

Guessing is fine when you are picking soup at a diner. It is not fine when you are picking health coverage.

The First Path: Original Medicare

Original Medicare includes Part A and Part B.

Part A helps cover hospital care.

Part B helps cover doctor visits, outpatient care, preventive services, and medically necessary services.

In 2026, the standard Medicare Part B premium is $202.90 per month, and the Part B deductible is $283. After the Part B deductible, you usually pay 20% of the Medicare-approved amount for covered services if your provider accepts assignment.

Original Medicare gives you broad provider access. In most cases, you can see any doctor or hospital that accepts Medicare.

That flexibility is one of the biggest reasons some seniors prefer Original Medicare.

But Original Medicare also has gaps.

It does not usually include prescription drug coverage, so many people add a separate Part D drug plan. It also does not usually cover routine dental, vision, or hearing care.

Many people who choose Original Medicare also consider a Medicare Supplement plan, also called Medigap, to help pay some out-of-pocket costs.

So Original Medicare may offer flexibility, but it may require separate pieces.

Think of it like ordering dinner à la carte. You can build what you want, but you need to know what is included and what costs extra.

The Second Path: Medicare Advantage

Medicare Advantage is also called Part C.

These plans are offered by private insurance companies approved by Medicare. Medicare Advantage plans must cover medically necessary services covered by Original Medicare, and many plans may offer extra benefits Original Medicare does not cover, such as dental, vision, hearing, fitness, transportation, and prescription drug coverage.

That can make Medicare Advantage attractive.

Many seniors like the idea of having hospital, medical, drug coverage, and extra benefits bundled into one plan.

But Medicare Advantage plans also have rules.

You may need to use doctors and hospitals in the plan network. You may need prior authorization before the plan covers certain services or supplies. Medicare explains that prior authorization is generally not required for Original Medicare in most cases, but may be required by Medicare Advantage plans.

That does not mean Medicare Advantage is bad.

It means you need to understand the tradeoff.

Medicare Advantage can offer convenience and extra benefits, but it may come with networks and approval rules.

Original Medicare can offer broad provider flexibility, but it may require separate drug and supplement coverage.

No path is perfect. The right path depends on your doctors, prescriptions, budget, travel habits, and comfort with networks.

The Question Is Not “Which One Is Better?”

This is where people get confused.

They ask, “Which is better, Original Medicare or Medicare Advantage?”

That is like asking, “Which is better, a pickup truck or a sedan?”

The answer is: better for what?

If you haul lumber every weekend, the pickup looks pretty good.

If you drive in city traffic and want easier parking, the sedan may make more sense.

Medicare works the same way.

The better question is:

Which Medicare path fits my life?

That means looking at your real situation.

Not your neighbor’s situation.

Not your cousin’s situation.

Not the plan your friend at the coffee shop loves.

Your situation.

Compare Your Doctors First

Before enrolling in a Medicare Advantage plan, check whether your doctors, specialists, hospitals, and preferred medical groups are in the plan network.

This is not something to assume.

Networks can change. Doctors can leave plans. Hospitals can have different arrangements.

If keeping your current doctors is important to you, this should be one of the first things you check.

With Original Medicare, you generally have broader access to providers who accept Medicare. With Medicare Advantage, access depends more on the plan’s network rules.

A plan with extra benefits may look attractive, but if your cardiologist is not in the network, that plan may suddenly look less attractive.

That is not a small detail. That is the whole ballgame.

Compare Your Prescriptions Next

Prescription drugs can make or break a Medicare plan.

In 2026, Medicare Part D has an important protection: yearly out-of-pocket costs for Part D-covered drugs are capped at $2,100. Once you reach that cap, you pay no copayment or coinsurance for covered Part D drugs for the rest of the calendar year.

That is good news.

But here is the catch: the cap applies to covered drugs.

You still need to check whether your prescriptions are on the plan’s formulary, what tier they are on, whether prior authorization applies, whether step therapy applies, and which pharmacies give you the best price.

Also, no Medicare drug plan may have a deductible higher than $615 in 2026, although some plans may have no deductible.

Do not simply ask, “Does this plan cover drugs?”

Ask:

“Does this plan cover my drugs?”

That one word, “my,” can save a lot of money.

Compare the Full Yearly Cost

Many people focus only on the monthly premium.

That is understandable. Premiums are easy to see.

But the real cost of a Medicare plan includes more than the monthly premium.

You should review:

Monthly premium

Deductible

Copays

Coinsurance

Drug costs

Maximum out-of-pocket limit

Dental costs

Vision costs

Hearing costs

Out-of-network costs

Expected specialist visits

Expected procedures

A zero-dollar premium does not mean zero cost.

It means zero-dollar premium.

There is a difference.

That is like saying the hotel room is free, but the bed, shower, towels, and electricity are extra. You would want to know that before checking in.

Watch the Extra Benefits

Medicare Advantage plans often advertise extra benefits.

Dental.

Vision.

Hearing.

Fitness.

Transportation.

Over-the-counter allowances.

Meal support.

These benefits can be useful. But the details matter.

A dental benefit may have an annual limit.

A hearing benefit may require you to use certain providers.

A vision benefit may only offer a limited eyewear allowance.

A transportation benefit may require advance scheduling.

An over-the-counter allowance may only work through approved catalogs or vendors.

The extra benefits are not the problem.

The problem is assuming they are unlimited.

They are usually not.

Read the details before you fall in love with the brochure.

Brochures are like dating profiles. They show you the best angles.

Travel Matters More Than People Think

If you travel often, your Medicare choice matters.

Original Medicare is widely accepted by providers across the country who accept Medicare.

Medicare Advantage plans may have networks, service areas, and out-of-network rules. Some PPO plans may allow out-of-network care, but you may pay more. Medicare explains that PPO plans have provider networks, and you generally pay less when using in-network providers.

This matters if you spend part of the year in another state, visit family often, or travel frequently.

A plan that works beautifully at home may be less convenient when you are away.

Before enrolling, ask how the plan works when you travel.

Do not wait until you are standing in a clinic three states away with a sore knee and a confused receptionist.

That is not the time to learn the rules.

Why Self-Enroll Gives Seniors More Control

Many seniors do not want to be rushed into a Medicare decision.

They want to compare.

They want to read.

They want to think.

They want to ask questions without feeling like someone is pushing them toward a plan.

That is the purpose of MedicareSelfEnroll.com.

The goal is to help seniors review options clearly, calmly, and with confidence.

You can compare plans based on your county, doctors, prescriptions, and needs.

You can look at the choices without the pressure.

That matters.

A Medicare decision should not feel like a race.

It should feel like a careful review.

The best Medicare choice is usually not made in panic. It is made by looking at the facts.

The Simple Medicare Decision Checklist

Before choosing between Original Medicare and Medicare Advantage in 2026, ask yourself:

Do I want broad provider flexibility?

Are my doctors in the plan network?

Are my hospitals in the plan network?

Are my prescriptions covered?

What are my total yearly costs?

Do I need dental, vision, or hearing benefits?

Do I travel often?

Am I comfortable with prior authorization rules?

Do I prefer bundled coverage or separate coverage pieces?

Can I afford the monthly premium and possible out-of-pocket costs?

This checklist will not make Medicare exciting.

Nothing can do that.

But it can make Medicare clearer.

And clear is what seniors need.

Final Thoughts

Original Medicare and Medicare Advantage are two different paths.

Original Medicare may offer broader provider flexibility, but it often requires separate drug coverage and possibly a Medigap plan.

Medicare Advantage may offer bundled coverage and extra benefits, but it may involve provider networks and prior authorization.

Neither path is automatically right or wrong.

The right choice is the one that fits your life.

Your doctors.

Your prescriptions.

Your budget.

Your health needs.

Your travel habits.

Your peace of mind.

At MedicareSelfEnroll.com, the mission is simple: help seniors compare Medicare options without pressure, confusion, or sales talk.

Because Medicare should not feel like a maze.

And seniors should not have to become insurance detectives just to choose a health plan.

FAQ Section

Is Medicare Advantage the same as Original Medicare?

No. Original Medicare is the federal Medicare program that includes Part A and Part B. Medicare Advantage, also called Part C, is offered by private insurance companies approved by Medicare. Medicare Advantage plans must cover medically necessary services covered by Original Medicare, but they may have different networks, costs, benefits, and rules.

Does Original Medicare require prior authorization?

In most cases, Original Medicare does not require prior authorization for covered services or supplies. Medicare Advantage plans may require prior authorization before covering certain services or items.

Do Medicare Advantage plans include prescription drug coverage?

Many Medicare Advantage plans include Part D prescription drug coverage, but not all do. You should check the plan details before enrolling.

What is the 2026 Medicare Part D out-of-pocket cap?

In 2026, yearly out-of-pocket costs for Part D-covered prescription drugs are capped at $2,100. Once you reach that cap, you pay no copayment or coinsurance for covered Part D drugs for the rest of the calendar year.

What is the maximum Part D deductible in 2026?

No Medicare drug plan may have a deductible higher than $615 in 2026. Some drug plans may have no deductible.

What is the Medicare Part B deductible in 2026?

The Medicare Part B deductible is $283 in 2026. The standard Part B premium is $202.90 per month.

Is Medicare Advantage better than Original Medicare?

Not automatically. Medicare Advantage may be better for some people, especially those who want bundled coverage and extra benefits. Original Medicare may be better for others who want broader provider flexibility. The right choice depends on your doctors, prescriptions, budget, travel habits, and health needs.

Can I compare Medicare plans online?

Yes. MedicareSelfEnroll.com helps seniors review Medicare options online in a clear, low-pressure way.

Is MedicareSelfEnroll.com affiliated with Medicare?

No. MedicareSelfEnroll.com is an independent insurance resource and is not affiliated with Medicare, Medicaid, or any U.S. government agency.

Read Other Blog:- Read Now

William Vargas brings over 50 years of financial and insurance expertise to every Medicare conversation. He operates MedicareSelfEnroll.com, helping seniors in Florida, New York, and North Carolina — with no pressure, no phone calls required.