In This Article

- What Does a Medicare Broker Do?

- What Does It Mean to Enroll Directly?

- The Biggest Advantage of Using a Broker

- The Biggest Advantage of Enrolling Directly

- The Problem With Pressure

- What About SHIP Counseling?

- Broker vs. Direct Enrollment: Which Is Better?

- Questions to Ask a Medicare Broker

- Questions to Ask Before Enrolling Directly

- The County-by-County Issue

- Where MedicareSelfEnroll.com Fits

- So, Should You Use a Broker or Enroll Directly?

- Final Takeaway

Choosing a Medicare plan is one of those decisions that looks simple from the outside — until you actually sit down and try to do it.

Then suddenly you are staring at Medicare Advantage plans, Part D drug plans, Medigap policies, premiums, deductibles, copays, provider networks, formularies, star ratings, dental benefits, vision benefits, hearing benefits, over-the-counter allowances, prior authorizations, and enough fine print to make your coffee go cold.

So the question becomes very real:

Should you use a Medicare broker, or should you enroll directly?

The honest answer is this: it depends on how comfortable you are comparing plans, how complicated your health and prescription needs are, and whether you trust the person helping you.

There is no one perfect answer for everybody. But there is one rule that applies to almost everyone:

Do not rush your Medicare decision.

Medicare.gov itself tells beneficiaries to compare plans available in their area, review costs and services, enter prescription drugs to estimate yearly costs, and consider talking to a trusted agent or broker before joining a plan.

That word trusted matters.

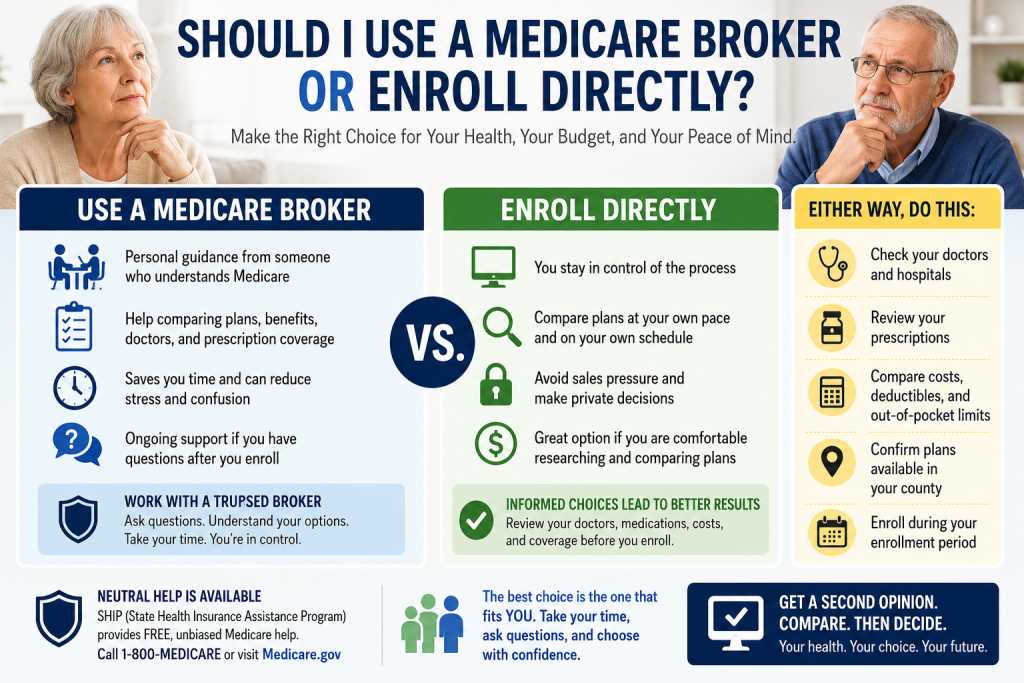

What Does a Medicare Broker Do?

A Medicare broker, sometimes called a Medicare agent, helps people compare and enroll in Medicare-related insurance options. This may include Medicare Advantage plans, Medicare Part D prescription drug plans, and Medicare Supplement plans, also called Medigap.

A good broker can help you understand:

What plans are available in your county

Whether your doctors are in network

Whether your prescriptions are covered

What your estimated costs may be

How Medicare Advantage differs from Original Medicare

Whether a Part D plan fits your medication list

Whether a Medigap plan may be worth considering

That can be very helpful, especially if you are new to Medicare or overwhelmed by all the choices.

But here is where seniors need to keep both eyes open.

A broker may not represent every plan in your area. Some brokers work with many insurance companies. Some work with only a few. Some may be excellent. Some may be rushed. Some may explain things clearly. Others may push the plan they are certified or paid to sell.

That does not mean brokers are bad. It means you need to ask questions.

What Does It Mean to Enroll Directly?

Enrolling directly means you choose and enroll in a plan without relying on a broker to guide the decision.

You may enroll directly through:

Medicare.gov

An insurance company website

A plan’s phone enrollment department

A self-service comparison and enrollment website

Paper enrollment forms

1-800-MEDICARE

Medicare.gov has an official Plan Finder that lets people compare Medicare health and drug plans in their area.

Direct enrollment gives you more control. You can move at your own pace, compare plans yourself, and avoid feeling pressured by a salesperson.

But direct enrollment also has a downside: you are responsible for understanding what you are choosing.

And Medicare is not exactly written like a diner menu. It is more like a tax form wearing a lab coat.

The Biggest Advantage of Using a Broker

The biggest advantage of using a broker is guidance.

A good broker can save you time and help you avoid mistakes. This is especially true if you have multiple prescriptions, several doctors, chronic conditions, or concerns about out-of-pocket costs.

For example, a plan may look attractive because it has a low premium. But if your doctor is not in network, or your medication is expensive under that plan, the “cheap” plan may become costly very quickly.

That is where a careful broker can help.

A good broker should ask questions before recommending anything:

What doctors do you want to keep?

What hospitals do you prefer?

What medications do you take?

Do you travel often?

Do you split time between states?

Do you care more about low premiums or broad provider access?

Are dental, vision, hearing, or OTC benefits important to you?

Are you comfortable with referrals or network restrictions?

If a broker starts talking before listening, be careful. That is not advice. That is a sales pitch warming up.

The Biggest Advantage of Enrolling Directly

The biggest advantage of enrolling directly is independence.

You are not sitting across from someone who may benefit from your enrollment. You can compare plans slowly, review the details, talk to family, check your doctors, and make a decision when you are ready.

Direct enrollment can be a good choice if:

You are comfortable using online tools

Your health needs are simple

You take few or no medications

You already know what kind of coverage you want

You want to avoid sales pressure

You want to compare plans privately before speaking with anyone

For many seniors, this is empowering. It puts the decision back where it belongs — in your hands.

But again, there is a catch.

If you miss an important detail, the consequences can follow you for the year. A wrong drug plan, a missing doctor, or a misunderstood network can create real frustration.

So direct enrollment is not “better” by itself. It is better only if you are willing to compare carefully.

The Problem With Pressure

Medicare decisions should not be made under pressure.

Unfortunately, many seniors receive phone calls, postcards, TV ads, emails, and online ads promising extra benefits, lower costs, or “free” services. Some of those messages are legitimate. Some are exaggerated. Some are misleading.

That is why a second opinion matters.

Before enrolling in any Medicare plan, you should feel comfortable saying:

“Let me compare.”

“Let me check my doctor.”

“Let me review my prescriptions.”

“Let me talk to someone I trust.”

“I am not ready to enroll today.”

If someone makes you feel rushed, that is a warning sign.

A good Medicare decision should feel clear, not pressured.

What About SHIP Counseling?

There is another option many people overlook: SHIP.

SHIP stands for State Health Insurance Assistance Program. Medicare.gov says SHIP provides free health insurance counseling to help people with Medicare choose a plan, review coverage, understand costs, apply for Extra Help, and make informed Medicare decisions.

Medicare also notes that SHIP programs are not connected to insurance companies or health plans.

That makes SHIP a useful resource, especially if you want a neutral review before making a decision.

However, SHIP counselors may not enroll you the same way a broker or online enrollment platform can. Their role is often educational and advisory. Still, they can be very helpful if you feel unsure.

Broker vs. Direct Enrollment: Which Is Better?

Here is the plain answer.

Use a broker if you want personal help, have complicated medical or prescription needs, or feel overwhelmed by the choices.

Enroll directly if you are comfortable comparing plans, want to avoid pressure, and prefer to make the final choice yourself.

Use SHIP if you want free, independent counseling and another set of eyes before making a decision.

The best path may actually be a combination:

Compare plans yourself.

Ask questions.

Speak with a trusted broker if needed.

Review with SHIP or someone you trust.

Then enroll only when you understand the plan.

That is the grown-up answer. Not flashy, but practical.

Questions to Ask a Medicare Broker

Before working with a broker, ask direct questions.

Do you represent all plans in my county, or only some?

Which insurance companies are you appointed with?

Are you licensed in my state?

How are you compensated?

Will you check my doctors and prescriptions?

Will you explain why you recommend a plan?

Can I review the information before enrolling?

Will you still help me after I enroll?

A trustworthy broker should not be offended by these questions.

If they get annoyed, that tells you something.

Questions to Ask Before Enrolling Directly

If you enroll directly, ask yourself:

Are my doctors in network?

Are my hospitals included?

Are my prescriptions covered?

What are the copays?

What is the maximum out-of-pocket cost?

Do I need referrals?

Are prior authorizations common?

Does the plan work if I travel?

Is this Medicare Advantage, Medigap, or Part D?

Am I enrolling at the right time?

Medicare Advantage plans are offered by private companies approved by Medicare, and most include drug coverage. Original Medicare includes Part A and Part B, and people can add a separate Part D plan and may buy supplemental coverage to help with out-of-pocket costs.

Those differences matter. You do not want to discover them after the doctor says, “We don’t take that plan.”

The County-by-County Issue

One of the most important Medicare details is this:

Plans vary by county.

A plan available in one county may not be available in another. Benefits may differ. Networks may differ. Drug coverage may differ. Premiums may differ.

That is why comparing county-by-county is so important.

A friend in another county may love their plan. That does not mean the same plan is available to you, or that it works the same way where you live.

Medicare is local in ways many people do not realize.

That is one reason a self-enrollment tool can be helpful. It allows you to compare options based on where you actually live, not based on someone else’s situation.

Where MedicareSelfEnroll.com Fits

MedicareSelfEnroll.com is built around a simple idea:

Second opinions come first.

The goal is not to rush seniors into a plan. The goal is to help people slow down, compare options, and enroll with more confidence.

That means:

You can review plans on your terms.

You can compare county-by-county.

You can avoid high-pressure sales tactics.

You can look before you leap.

You can ask questions before making a decision.

This is especially valuable for seniors who do not want to be pushed by phone calls but also do not want to feel abandoned in a maze of Medicare choices.

So, Should You Use a Broker or Enroll Directly?

Here is the final answer.

If you trust the broker, and the broker takes time to understand your needs, a broker can be very helpful.

If you want control, privacy, and time to compare, direct enrollment may be a better fit.

But either way, do not make the decision blind.

Do not choose a plan just because of a TV commercial.

Do not choose a plan just because a friend likes it.

Do not choose a plan just because someone called you.

Do not choose a plan just because the premium looks low.

Do not choose a plan until you check doctors, drugs, costs, and county availability.

Medicare is not a race. There is no prize for enrolling too fast.

The prize is choosing a plan that actually fits your life.

Final Takeaway

A Medicare broker can be useful. Direct enrollment can be empowering. SHIP counseling can provide independent help. The real mistake is not which path you choose — the real mistake is rushing into a plan without understanding it.

So take your time.

Compare carefully.

Get a second opinion.

And when you are ready, enroll with confidence — not pressure.

MedicareSelfEnroll.com is an independent insurance resource and is not affiliated with Medicare, Medicaid, or any U.S. government agency.

William Vargas brings over 50 years of financial and insurance expertise to every Medicare conversation. He operates MedicareSelfEnroll.com, helping seniors in Florida, New York, and North Carolina — with no pressure, no phone calls required.