In This Article

- What Is the Medicare Initial Enrollment Period?

- Why Missing Your IEP Can Be So Expensive

- The Medicare Part B Late-Enrollment Penalty

- Example of a Part B Penalty

- The Medicare Part D Late-Enrollment Penalty

- Example of a Part D Penalty

- “I Don’t Take Any Medications” Is Not a Strategy

- What If You Are Still Working at 65?

- What Is Creditable Drug Coverage?

- Part A Can Also Have a Penalty for Some People

- Why Medicare Penalties Feel So Unfair

- How to Avoid Medicare Late-Enrollment Penalties

- What If You Already Missed Your IEP?

- The Bottom Line

Most people think Medicare begins automatically and everything will somehow fall into place.

That is a dangerous assumption.

Medicare has rules. Medicare has deadlines. And if you miss certain deadlines, the penalty may not be temporary. It may follow you for the rest of your life, like a bad financial mosquito that never stops buzzing.

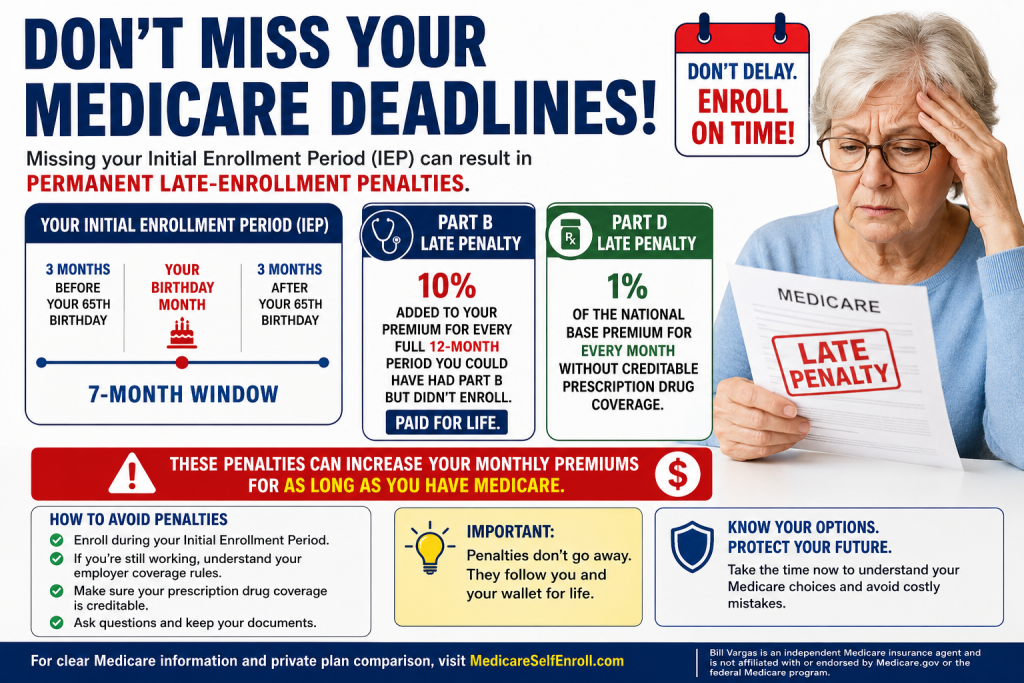

One of the most important deadlines is your Initial Enrollment Period, often called your IEP. This is the first window of time when most people can sign up for Medicare. For most people, it begins three months before the month they turn 65, includes their birthday month, and continues for three months after. In total, it is a seven-month window. Medicare warns that if you miss this period, you may have to wait to sign up and may pay a late enrollment penalty for as long as you have Part B.

That is why this matters so much.

A missed deadline is not just paperwork. It can become a permanent monthly expense.

What Is the Medicare Initial Enrollment Period?

Your Medicare Initial Enrollment Period is your first opportunity to enroll in Medicare when you become eligible, usually around your 65th birthday.

For most people, the IEP lasts seven months:

Three months before your 65th birthday month, your birthday month, and three months after your birthday month.

For example, if you turn 65 in July, your Initial Enrollment Period generally begins April 1 and ends October 31.

This is the time to make important decisions about Medicare Part A, Part B, Part D, Medicare Advantage, or Medicare Supplement coverage.

Some people are automatically enrolled in Medicare if they are already receiving Social Security benefits. Others must actively sign up. That is where people get into trouble. They assume Medicare will “just happen,” and then later discover that Medicare does not run on assumptions.

Why Missing Your IEP Can Be So Expensive

The biggest danger in missing your Initial Enrollment Period is that Medicare may charge late-enrollment penalties.

These penalties are not like a parking ticket. You do not just pay once and move on.

For many people, the penalty becomes part of the monthly premium. Month after month. Year after year. Sometimes for life.

The two penalties seniors need to understand clearly are the Part B late-enrollment penalty and the Part D late-enrollment penalty.

Part B covers doctor services, outpatient care, preventive services, durable medical equipment, and many medically necessary services.

Part D covers prescription drugs, either through a standalone drug plan or through a Medicare Advantage plan that includes drug coverage.

Missing either one can become expensive.

The Medicare Part B Late-Enrollment Penalty

The Part B penalty is one of the most misunderstood Medicare penalties.

If you do not sign up for Medicare Part B when you are first eligible, and you do not qualify for a Special Enrollment Period, your monthly Part B premium may go up by 10% for each full 12-month period you could have had Part B but did not enroll. CMS says this penalty may last for as long as you have Medicare.

Let’s put that in plain English.

If you delayed Part B for one full year, your Part B premium may be 10% higher.

If you delayed for two full years, your premium may be 20% higher.

If you delayed for three full years, your premium may be 30% higher.

And this is not just for one year. Medicare says the penalty can last as long as you have Part B coverage.

That is the part that makes people sit up straight.

A person may think, “I missed the deadline. I’ll just fix it later.”

Yes, you may be able to fix the enrollment problem later. But the penalty may not disappear.

Example of a Part B Penalty

Let’s say someone should have enrolled in Part B at age 65 but waited until age 67. That could be two full 12-month periods without Part B.

That person may face a 20% penalty added to the standard Part B premium.

Medicare gives an example using the 2026 standard Part B premium of $202.90. A 20% late-enrollment penalty would add $40.58, bringing the monthly amount to $243.48.

Now ask yourself this: would you willingly pay extra every month for the rest of your life because of a missed deadline?

Of course not.

But many people end up doing exactly that because they did not understand the rules.

The Medicare Part D Late-Enrollment Penalty

The Part D penalty works differently from the Part B penalty, but it can also become a long-term monthly cost.

Medicare Part D is prescription drug coverage. You can get it through a standalone Part D plan or through a Medicare Advantage plan that includes prescription drug coverage.

The Part D late-enrollment penalty generally applies if you go without Medicare drug coverage or other creditable prescription drug coverage for 63 days or more after your Initial Enrollment Period ends.

Creditable coverage means prescription drug coverage that is expected to pay, on average, at least as much as standard Medicare drug coverage.

Here is the basic formula: Medicare calculates the Part D penalty by multiplying 1% of the national base beneficiary premium by the number of full, uncovered months you went without Part D or other creditable drug coverage. For 2026, Medicare lists the national base beneficiary premium as $38.99.

That amount is then rounded and added to your monthly Part D premium.

And here is the kicker: the national base beneficiary premium can change each year, so the dollar amount of your penalty can also change.

Example of a Part D Penalty

Let’s say someone went 20 full months without creditable prescription drug coverage after becoming eligible for Medicare.

The calculation would be:

1% × $38.99 × 20 months

That equals about $7.80 per month in 2026.

Now, $7.80 may not sound like much. That is how Medicare gets you. It looks small.

But over time, it adds up. And if the person lives another 20 years, that small monthly penalty becomes a needless long-term expense.

It is like a leaky faucet. One drip does not scare anybody. But leave it alone long enough and suddenly you are wondering why the water bill looks like it joined a country club.

“I Don’t Take Any Medications” Is Not a Strategy

Many healthy 65-year-olds make this mistake.

They say, “I do not take any prescriptions, so I do not need a drug plan.”

That sounds reasonable.

But Medicare does not base the Part D penalty on whether you needed medication. Medicare bases it on whether you had creditable drug coverage.

You may be healthy today. Wonderful. Celebrate that. Take a walk. Eat your oatmeal. Call your cousin.

But tomorrow is not guaranteed. You may need medication later. And if you delayed Part D without other creditable coverage, you may have to pay a penalty when you finally enroll.

This is why many people choose a low-cost Part D plan even if they take no prescriptions. They are not buying it because they love insurance paperwork. They are buying it to protect themselves from penalties and future drug costs.

What If You Are Still Working at 65?

This is where Medicare gets tricky.

Some people can delay Medicare Part B without penalty if they are covered by a current employer group health plan based on active employment. This may apply if you or your spouse is still working and you have qualifying employer coverage.

But do not guess.

This is one of the biggest Medicare danger zones.

Retiree coverage, COBRA, marketplace coverage, VA benefits, and employer coverage from a small company may not protect you the same way active employer coverage from a larger employer might.

This is where people get burned.

They think, “I have insurance, so I’m fine.”

Maybe. Maybe not.

The real question is not simply whether you have coverage. The real question is whether Medicare considers that coverage valid for delaying Medicare without penalty.

That is a very different question.

What Is Creditable Drug Coverage?

For Part D, the magic word is creditable.

If you have prescription drug coverage from an employer, union, retiree plan, VA, TRICARE, or another source, you should receive a notice telling you whether that coverage is creditable.

Do not throw that notice away.

That notice may be your proof that you had coverage good enough to avoid a Part D penalty.

If you ever lose that coverage and later enroll in Medicare drug coverage, Medicare may ask whether you had creditable coverage. Having documentation can help you avoid a penalty that should not apply.

In plain language: keep the paperwork.

Yes, paperwork is annoying. But so is paying a lifetime penalty because you tossed the one letter that could have saved you.

Part A Can Also Have a Penalty for Some People

Most people get Medicare Part A premium-free because they or their spouse worked and paid Medicare taxes long enough.

But not everyone qualifies for premium-free Part A.

If you have to buy Part A and you do not sign up when first eligible, you may also face a Part A late-enrollment penalty. This does not apply to most people, but it matters for those who are not eligible for premium-free Part A.

For this article, the main focus is Part B and Part D because those are the penalties many seniors are more likely to face.

Why Medicare Penalties Feel So Unfair

The frustrating thing about Medicare late-enrollment penalties is that many people do not miss deadlines on purpose.

They miss them because Medicare is confusing.

They are still working.

They think their employer coverage is enough.

They assume Social Security will handle everything.

They believe Medicare Advantage includes everything automatically.

They do not take prescriptions and skip Part D.

They moved, retired, lost coverage, or misunderstood a letter.

In other words, people make normal human mistakes inside a system that does not always explain itself clearly.

But Medicare does not care that you were confused. Medicare follows rules.

And that is why education matters.

How to Avoid Medicare Late-Enrollment Penalties

The first step is knowing your dates.

If you are turning 65, write down your Initial Enrollment Period. Do not keep it floating around in your head next to grocery lists, birthday reminders, and “Where did I put my glasses?”

Put it on a calendar.

The second step is confirming your current coverage.

Ask your employer benefits department whether your coverage allows you to delay Medicare Part B without penalty. Get the answer in writing if possible.

The third step is checking your prescription drug coverage.

Ask whether your drug coverage is creditable. Keep the annual creditable coverage notice.

The fourth step is not waiting until the last minute.

Medicare enrollment is not something to handle while standing in line at the supermarket or while the grandkids are asking for the Wi-Fi password.

Give yourself time.

The fifth step is reviewing all your options.

You may need Original Medicare, a Medicare Supplement, a Part D plan, or a Medicare Advantage plan. The right answer depends on your doctors, prescriptions, budget, health needs, travel patterns, and personal preferences.

What If You Already Missed Your IEP?

If you already missed your Initial Enrollment Period, do not panic — but do not ignore it either.

You may still have options.

Depending on your situation, you may qualify for a Special Enrollment Period. For example, if you delayed Part B because you had qualifying employer coverage based on current employment, you may be able to enroll later without a penalty.

If you do not qualify for a Special Enrollment Period, you may have to wait for another enrollment window.

The important thing is to act quickly and get accurate information.

The longer you wait, the worse the penalty may become.

Medicare penalties are like weeds in the garden. Ignore them, and they do not politely go away. They spread.

The Bottom Line

Missing your Medicare Initial Enrollment Period can be costly.

The Part B penalty can add 10% to your monthly premium for every full 12-month period you delayed enrollment without qualifying coverage, and it may last as long as you have Part B.

The Part D penalty can add 1% of the national base beneficiary premium for every full uncovered month you went without Medicare drug coverage or other creditable prescription drug coverage. For 2026, that base premium is $38.99.

That is why the safest approach is simple: know your enrollment window, verify your coverage, keep your documents, and do not assume everything will work itself out.

Medicare is not something to guess your way through.

A missed deadline today can become a monthly bill tomorrow.

And in Elderhood, the goal is not to give Medicare extra money because of confusion. The goal is to protect your health, your independence, and your wallet.

For clear Medicare information and private plan comparison, visit MedicareSelfEnroll.com.

Bill Vargas is an independent Medicare insurance agent and is not affiliated with or endorsed by Medicare.gov or the federal Medicare program.

William Vargas brings over 50 years of financial and insurance expertise to every Medicare conversation. He operates MedicareSelfEnroll.com, helping seniors in Florida, New York, and North Carolina — with no pressure, no phone calls required.