In This Article

- What Is Medicare Advantage Open Enrollment?

- Who Can Use This Enrollment Period?

- Why Would Someone Change Plans After January 1?

- What Should You Check Before Switching?

- What If You Want to Go Back to Original Medicare?

- Medicare Advantage Plans Can Have Prior Authorization

- Do Not Choose a Plan Based Only on Extra Benefits

- What Happens After You Make a Change?

- Why MedicareSelfEnroll.com Exists

- Final Thought

- What is Medicare Advantage Open Enrollment?

- Can anyone use Medicare Advantage Open Enrollment?

- Can I switch from Original Medicare to Medicare Advantage during this period?

- Can I change my Part D drug plan during this period?

- How many changes can I make during Medicare Advantage Open Enrollment?

- Should I switch Medicare Advantage plans if my doctor is not in network?

- Can I return to Original Medicare and get Medigap?

- Is MedicareSelfEnroll.com affiliated with Medicare?

Medicare has a way of making simple things feel like a puzzle with half the pieces missing.

You choose a plan. You think you are done. Then January arrives and something does not feel right.

Maybe your doctor is no longer in network. Maybe your prescription costs more than expected. Maybe your specialist visit has a higher copay. Maybe the plan sounded wonderful in October, but now that you are actually using it, the shine has worn off.

That is where the Medicare Advantage Open Enrollment Period becomes important.

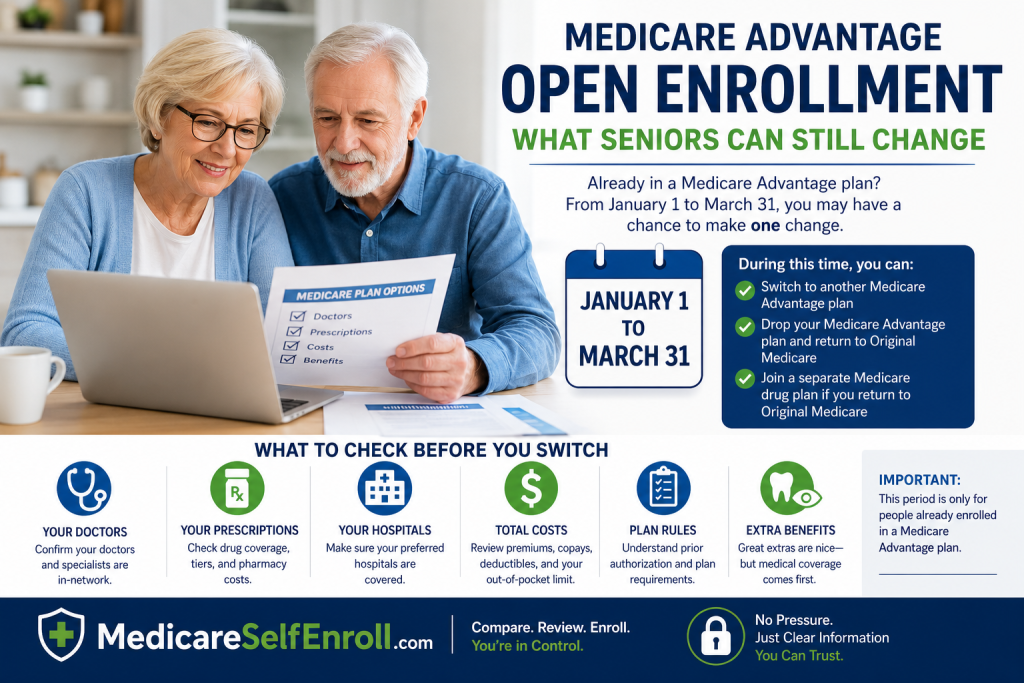

This period runs from January 1 through March 31 each year, but it is only for people who are already enrolled in a Medicare Advantage plan. During this time, Medicare says you can switch to another Medicare Advantage plan, with or without drug coverage, or drop your Medicare Advantage plan and return to Original Medicare. You can also join a separate Medicare drug plan if you return to Original Medicare.

This is not a second chance for everyone. It is a specific window with specific rules.

And for seniors, knowing the difference can prevent a costly mistake.

What Is Medicare Advantage Open Enrollment?

Medicare Advantage Open Enrollment is a special enrollment window for people who already have a Medicare Advantage plan.

It runs from January 1 to March 31.

During this period, you can make one change if you are already in a Medicare Advantage plan.

You can:

Switch from one Medicare Advantage plan to another Medicare Advantage plan.

Drop your Medicare Advantage plan and return to Original Medicare.

Join a separate Medicare Part D prescription drug plan if you return to Original Medicare.

That is the basic idea.

But here is the important part: this period is not the same as the fall Medicare Open Enrollment Period.

The fall Open Enrollment Period runs from October 15 to December 7, and changes made during that period take effect January 1 of the following year.

The January-to-March period is more limited.

Think of fall Open Enrollment as the big Medicare shopping season.

Think of Medicare Advantage Open Enrollment as the “something went wrong, let me fix this if I can” season.

Not elegant, but accurate.

Who Can Use This Enrollment Period?

This period is only for people who are already enrolled in a Medicare Advantage plan.

If you have Original Medicare only, this period does not allow you to join Medicare Advantage for the first time.

If you have Original Medicare with a standalone Part D plan, this period does not allow you to switch Part D plans just because you feel like shopping around.

Medicare explains that during the Medicare Advantage Open Enrollment Period, you cannot switch from Original Medicare to a Medicare Advantage plan, join a separate drug plan if you have Original Medicare, or switch from one standalone drug plan to another if you have Original Medicare.

That is where many people get confused.

Medicare uses similar-sounding names for different enrollment windows. It is like naming every grandchild “Jimmy” and then wondering why Thanksgiving is chaos.

So remember this:

If you are already in Medicare Advantage, this period may help you.

If you are not already in Medicare Advantage, this particular window probably does not apply to you.

Why Would Someone Change Plans After January 1?

Most people do not change Medicare plans for fun.

They change because something is not working.

Common reasons include:

Your doctor is not in the network.

Your hospital is not covered the way you expected.

Your prescriptions cost more than you thought.

Your pharmacy is not preferred.

You are unhappy with prior authorization rules.

A specialist referral is harder than expected.

Your copays are higher than you planned.

You misunderstood what the plan actually covered.

Sometimes the problem is not obvious until you start using the plan.

A Medicare Advantage plan may look fine on paper. But real life is not paper.

Real life is the cardiologist appointment, the pharmacy counter, the knee injection, the MRI, the lab bill, and the doctor’s office saying, “We do not take that plan anymore.”

That is when seniors need to stop and review their options.

What Should You Check Before Switching?

Before changing from one Medicare Advantage plan to another, slow down and compare carefully.

Do not switch just because a plan sounds better in an ad.

Check your actual needs.

Start with your doctors.

Are your primary doctor and specialists in the new plan’s network?

Then check hospitals.

Is your preferred hospital included?

Then check prescriptions.

Are your medications covered? What tier are they on? Do they require prior authorization or step therapy?

Then check pharmacies.

Is your regular pharmacy a preferred pharmacy under the plan?

Then check costs.

Look at the premium, copays, deductibles, specialist visits, hospital costs, and maximum out-of-pocket limit.

The lowest monthly premium is not always the lowest total cost.

That is one of the biggest Medicare traps.

A zero-premium plan may still have copays, drug costs, network limits, and prior authorization rules.

Free is a wonderful word. But in Medicare, it needs a magnifying glass.

What If You Want to Go Back to Original Medicare?

During Medicare Advantage Open Enrollment, you may be able to drop your Medicare Advantage plan and return to Original Medicare.

You may also be able to join a standalone Part D prescription drug plan.

But there is a serious issue seniors need to understand:

Returning to Original Medicare does not automatically mean you can get a Medicare Supplement, also called Medigap, at the price or approval you want.

Medigap rules vary by state. In many situations, outside your Medigap Open Enrollment Period or certain guaranteed issue rights, insurers may use medical underwriting. That means health conditions can affect whether you are accepted and what you pay.

This is one of those details that can bite people.

A senior may think, “I’ll just go back to Original Medicare and get a supplement.”

Maybe.

Maybe not.

Before leaving Medicare Advantage, check whether you can get a Medigap policy if you want one. In some states, you have stronger protections. In others, your options may be more limited.

This is not a small technicality. It can affect your healthcare costs for years.

Medicare Advantage Plans Can Have Prior Authorization

Another issue seniors should understand is prior authorization.

Prior authorization means the plan may need to approve certain services before they are covered.

This can apply to imaging, procedures, rehab services, medical equipment, or other types of care.

Medicare’s 2026 handbook notes that some Medicare Advantage services may require approval from the plan before they are covered.

That does not mean every prior authorization is bad.

But it does mean seniors should know the rules before enrolling.

If you need ongoing medical care, specialist treatment, therapy, or expensive medications, prior authorization rules can matter a lot.

A plan may have good extra benefits, but if care is delayed or harder to access, those extras may not feel very comforting.

Dental benefits are nice. Vision benefits are nice. A gym membership is nice.

But if you are waiting for approval on something important, the free gym bag is not going to cheer you up.

Do Not Choose a Plan Based Only on Extra Benefits

Medicare Advantage plans often promote extra benefits.

Dental. Vision. Hearing. Transportation. Over-the-counter allowances. Fitness programs.

Some of these benefits can be useful.

But they should never distract from the basics.

Your first questions should always be:

Are my doctors covered?

Are my hospitals covered?

Are my prescriptions covered?

What will my care cost?

What is my maximum out-of-pocket risk?

Are prior authorizations required?

Extras are fine, but medical coverage is the foundation.

Choosing a Medicare plan because of extras alone is like buying a house because you like the welcome mat.

The welcome mat is nice.

The roof matters more.

What Happens After You Make a Change?

During the Medicare Advantage Open Enrollment Period, you can generally make one change.

Medicare states that changes made during this period are effective the first day of the month after the plan gets your request.

That means timing matters.

Do not wait until the last minute if you already know your plan is not working.

But also do not rush.

A rushed Medicare decision can create a different problem.

The best approach is simple:

Review your current problem.

Compare your available options.

Confirm doctors and prescriptions.

Check total costs.

Understand what you are giving up.

Then decide.

That is how seniors protect themselves.

Why MedicareSelfEnroll.com Exists

MedicareSelfEnroll.com was created for seniors who want to compare Medicare options without pressure.

The purpose is not to scare people into switching.

The purpose is to help people understand their choices.

Some seniors are happy with their Medicare Advantage plan.

Some should consider another plan.

Some may prefer Original Medicare.

Some may want to explore Medigap.

The point is not that one choice is right for everyone.

The point is that your choice should fit your doctors, prescriptions, budget, and personal needs.

Medicare should not be a guessing game.

And it should not feel like someone is trying to sell you a used car in a hurricane.

Final Thought

Medicare Advantage Open Enrollment gives some seniors a chance to correct a plan choice that is not working.

But it has limits.

It is only for people already enrolled in Medicare Advantage.

It generally allows one change.

It does not give everyone the same options as fall Open Enrollment.

And it should not be used casually.

Before switching, check your doctors, hospitals, prescriptions, pharmacies, costs, and prior authorization rules.

Do not assume.

Do not rush.

Do not choose based only on commercials or extra benefits.

Your Medicare plan should fit your real life.

That is the whole point.

FAQ

What is Medicare Advantage Open Enrollment?

Medicare Advantage Open Enrollment is a yearly period from January 1 through March 31 for people already enrolled in a Medicare Advantage plan. During this period, they may switch to another Medicare Advantage plan or return to Original Medicare.

Can anyone use Medicare Advantage Open Enrollment?

No. This period is only for people who are already enrolled in a Medicare Advantage plan. It is not for people with Original Medicare who want to join Medicare Advantage for the first time.

Can I switch from Original Medicare to Medicare Advantage during this period?

No. Medicare says you cannot switch from Original Medicare to a Medicare Advantage plan during the Medicare Advantage Open Enrollment Period.

Can I change my Part D drug plan during this period?

Only in certain situations. If you drop Medicare Advantage and return to Original Medicare, you can generally join a separate Medicare drug plan. But if you already have Original Medicare with a standalone Part D plan, this period does not let you switch from one standalone drug plan to another.

How many changes can I make during Medicare Advantage Open Enrollment?

Generally, you can make one change during this period. Any change you make usually becomes effective the first day of the month after the plan receives your request.

Should I switch Medicare Advantage plans if my doctor is not in network?

You should review your options carefully. If your doctor or specialist is no longer in network, switching plans may make sense, but you should confirm doctors, hospitals, prescriptions, pharmacies, and total costs before making a change.

Can I return to Original Medicare and get Medigap?

You may return to Original Medicare during this period, but getting a Medigap policy may depend on your state, timing, health history, and whether you have guaranteed issue rights. Check Medigap availability before leaving Medicare Advantage.

Is MedicareSelfEnroll.com affiliated with Medicare?

No. MedicareSelfEnroll.com is an independent educational and plan comparison resource. It is not affiliated with the federal Medicare program.

Read Other Blog:- Read Now

William Vargas brings over 50 years of financial and insurance expertise to every Medicare conversation. He operates MedicareSelfEnroll.com, helping seniors in Florida, New York, and North Carolina — with no pressure, no phone calls required.