In This Article

- Why Medicare Plan Comparison Matters in 2026

- Original Medicare vs. Medicare Advantage

- Do Not Choose a Plan Just Because the Premium Is Low

- Your Doctors Matter

- Your Prescriptions Matter Too

- Prior Authorization: The Fine Print Seniors Should Understand

- Star Ratings Can Help, But They Are Not the Whole Story

- Why Self-Enroll Can Be Better Than Being Rushed

- A Simple Medicare Plan Checklist for 2026

- The Bottom Line

- What is the best Medicare plan for 2026?

- Should I choose Original Medicare or Medicare Advantage?

- What should I check before enrolling in a Medicare Advantage plan?

- Are $0 premium Medicare Advantage plans really free?

- Can Medicare Advantage plans change every year?

- What is prior authorization?

- Where can I compare Medicare plans?

- Why use MedicareSelfEnroll.com?

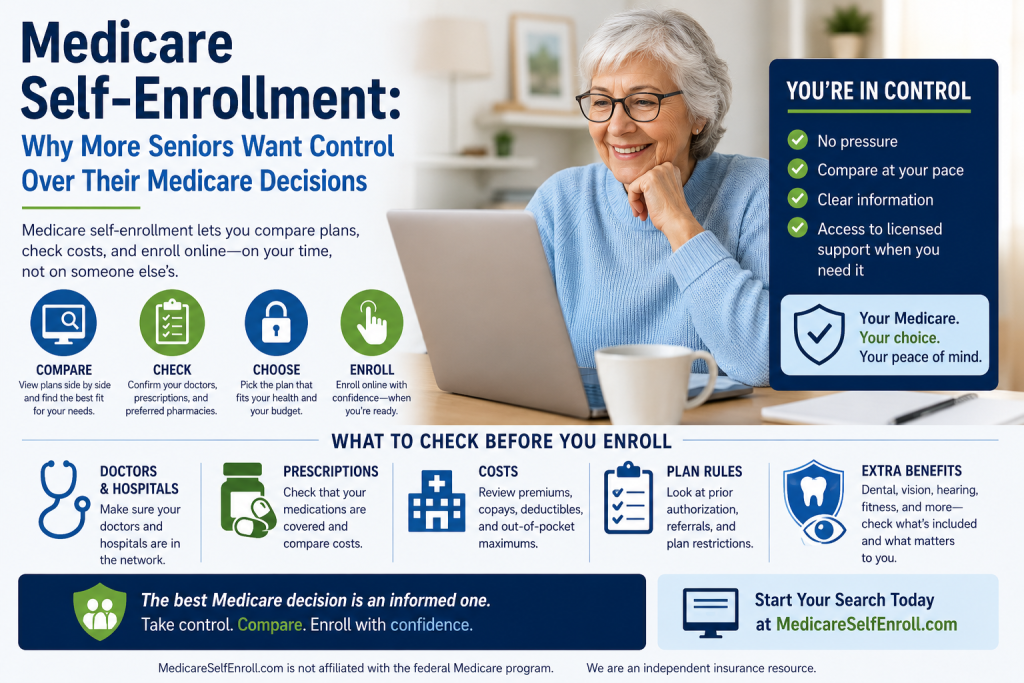

Choosing a Medicare plan should not feel like trying to solve a crossword puzzle while someone is yelling at you on the phone.

Yet that is exactly how many people feel.

You turn 65, or you are already on Medicare, and suddenly the mail starts coming. Then the phone calls. Then the TV commercials. Then the online ads promising benefits that sound wonderful, but leave out the fine print.

That is why MedicareSelfEnroll.com was created around one simple idea:

You should be able to compare Medicare plans calmly, clearly, and without pressure.

Why Medicare Plan Comparison Matters in 2026

Medicare plans can change every year.

Premiums can change. Drug coverage can change. Doctor networks can change. Copays can change. Prior authorization rules can change. Extra benefits can change.

That means the plan that worked well last year may not be the best fit this year.

Medicare.gov explains that when comparing Original Medicare and Medicare Advantage, people should look at doctor choice, hospital access, costs, coverage, and travel needs before deciding. That is the plain truth. The right plan depends on your life, not someone else’s sales pitch.

Original Medicare vs. Medicare Advantage

Original Medicare includes Part A and Part B.

With Original Medicare, you can generally use any doctor or hospital in the United States that accepts Medicare. Many people also add a separate Part D prescription drug plan and may consider a Medicare Supplement, also called Medigap, to help with out-of-pocket costs. Medicare.gov states that Original Medicare includes Part A and Part B, and people can join a separate Part D plan for drug coverage.

Medicare Advantage, also called Part C, is different.

These plans are offered by private insurance companies approved by Medicare. Many Medicare Advantage plans include prescription drug coverage and may offer extra benefits such as dental, vision, hearing, fitness, transportation, or over-the-counter allowances.

That sounds attractive, and sometimes it is. But there is a catch.

Medicare Advantage plans usually have networks, rules, copays, and sometimes prior authorization requirements. Medicare.gov notes that Medicare Advantage members typically need prior authorization before certain services or supplies are covered.

That does not mean Medicare Advantage is bad. It means you need to compare carefully.

Do Not Choose a Plan Just Because the Premium Is Low

A $0 premium Medicare Advantage plan can sound like a gift.

But here is the question: what happens when you actually need care?

A low premium does not automatically mean low total cost. You still need to check:

Your doctor network

Your hospital network

Specialist access

Prescription drug coverage

Copays

Deductibles

Maximum out-of-pocket costs

Dental, vision, and hearing limits

Travel coverage

Prior authorization requirements

A plan can look great in a commercial and still be wrong for your real life.

That is why self-enrollment should never mean guessing. It should mean comparing carefully before choosing.

Your Doctors Matter

For many seniors, keeping their doctor is one of the most important parts of choosing a Medicare plan.

Before enrolling in any Medicare Advantage plan, check whether your primary doctor, specialists, hospitals, and preferred pharmacies are in the plan’s network.

Do not assume.

Networks can change. A doctor who accepted one plan last year may not accept the same plan this year. A specialist may be in one plan’s network but not another.

If your doctor matters to you, verify first.

Your Prescriptions Matter Too

Prescription drug costs can surprise people.

A medication that was affordable last year may move to a higher tier. A plan may change its formulary. A preferred pharmacy may no longer offer the best pricing. A deductible may apply before your drug coverage begins.

Medicare.gov’s Plan Compare tool allows people to enter their ZIP code and compare health and drug plans in their area, including costs. This is one of the most important steps in choosing wisely.

Do not just ask, “Does this plan cover drugs?”

Ask, “Does this plan cover my drugs, at my pharmacy, at a price I can live with?”

That is the difference between shopping and hoping.

Prior Authorization: The Fine Print Seniors Should Understand

Prior authorization means the plan may require approval before it covers certain services, supplies, or medications.

This can include imaging, procedures, equipment, medications, therapy, or other medical services.

Again, prior authorization is not automatically bad. But it is something seniors should understand before enrolling.

If you have ongoing health needs, expensive medications, mobility issues, cancer treatment, cardiac care, diabetes care, or other regular medical needs, plan rules matter.

You do not want to discover the rules after you are already sick.

Star Ratings Can Help, But They Are Not the Whole Story

Medicare Star Ratings are designed to help people compare Medicare Advantage and Part D plans based on quality and performance. CMS explains that the Star Ratings system gives beneficiaries quality and performance information to help them choose health and drug coverage during fall open enrollment.

That is useful.

But do not choose a plan based only on stars.

A plan can have a good rating and still not include your doctor. A plan can look strong overall and still not cover your specific prescription well.

Star Ratings are a helpful signal. They are not a substitute for checking your personal needs.

Why Self-Enroll Can Be Better Than Being Rushed

There is nothing wrong with getting help from a licensed agent.

But there is something wrong with feeling pressured, rushed, confused, or talked into a plan you do not fully understand.

Self-enrollment gives you time to slow down.

You can compare plans. You can check your doctors. You can review your drugs. You can look at costs. You can think.

That matters because Medicare is not just paperwork. It affects your health, your money, and your peace of mind.

At MedicareSelfEnroll.com, the goal is simple:

No pressure. No confusion. Just a clear path to compare Medicare options and enroll with confidence.

A Simple Medicare Plan Checklist for 2026

Before choosing a Medicare plan, ask yourself:

Are my doctors in the plan?

Are my hospitals in the plan?

Are my prescriptions covered?

What will my medications cost?

What is the monthly premium?

What are the copays?

What is the maximum out-of-pocket cost?

Do I need referrals?

Does the plan require prior authorization?

Does the plan fit how I actually live?

That last question may be the most important one.

Because the best Medicare plan is not the one with the loudest commercial.

It is the one that fits your health, your doctors, your prescriptions, your budget, and your life.

The Bottom Line

Medicare plan shopping in 2026 does not have to be scary.

But it does require attention.

Do not let commercials, postcards, or phone calls make the decision for you. Compare your options. Check the details. Look beyond the monthly premium. Make sure your doctors, drugs, and hospitals fit the plan before you enroll.

Self-enrollment is not about being alone.

It is about being informed.

And when you are informed, you are much harder to confuse.

That is the MedicareSelfEnroll.com way.

FAQ: Comparing Medicare Plans in 2026

What is the best Medicare plan for 2026?

There is no single best Medicare plan for everyone. The best plan depends on your doctors, prescriptions, budget, health needs, location, and whether you prefer Original Medicare or Medicare Advantage.

Should I choose Original Medicare or Medicare Advantage?

Original Medicare may offer broader provider access because you can generally use any doctor or hospital that accepts Medicare. Medicare Advantage may offer extra benefits, but often uses networks and plan rules. The right choice depends on your personal needs.

What should I check before enrolling in a Medicare Advantage plan?

Check your doctors, hospitals, prescriptions, pharmacy, copays, deductibles, maximum out-of-pocket cost, referral rules, and prior authorization requirements.

Are $0 premium Medicare Advantage plans really free?

No. A $0 premium means you may not pay an additional monthly plan premium, but you may still have copays, deductibles, coinsurance, drug costs, and out-of-pocket limits.

Can Medicare Advantage plans change every year?

Yes. Medicare Advantage plans can change premiums, benefits, networks, drug coverage, copays, and other rules each year. That is why reviewing your plan annually is important.

What is prior authorization?

Prior authorization means the plan may require approval before covering certain services, supplies, or medications. Medicare.gov notes that Medicare Advantage plans typically require prior authorization for some covered services or supplies.

Where can I compare Medicare plans?

You can compare Medicare health and drug plans using the official Medicare Plan Compare tool. Medicare.gov allows users to enter their ZIP code and compare available plans in their area.

Why use MedicareSelfEnroll.com?

MedicareSelfEnroll.com is designed to help seniors compare Medicare options without pressure. The goal is to make Medicare enrollment clearer, calmer, and easier to understand.

Read Other Blog:- Read Now

William Vargas brings over 50 years of financial and insurance expertise to every Medicare conversation. He operates MedicareSelfEnroll.com, helping seniors in Florida, New York, and North Carolina — with no pressure, no phone calls required.